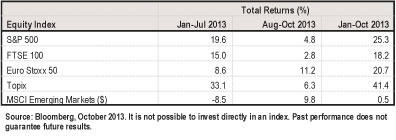

Two performance trends have stood out across world markets during 2013. The first is the strong outperformance by equities over bonds. The second is the strong returns of the U.S. stock market relative to other stock markets around the world. The Table breaks down year to date performance for the S&P 500, Eurostoxx 50, FTSE 100, Topix and MSCI Emerging Market indices. Notice that as of the end of July, equity returns in the Unites States were handily outpacing all other regions except Japan.

We now expect non-U.S. equity markets to begin to close the performance gap that opened during the first half of this year. Our expectation is a consistent conclusion across two types of analysis. The first is a static valuation analysis which reveals that U.S. markets are more expensive than many non-U.S. markets following this strong outperformance. For example, according to Morgan Stanley Capital International data, both the developed markets (as measured by EAFE) and the emerging markets (as measured by the MSCI Emerging Markets index) offer higher earnings yields and cash flow yields than U.S. equities. The second analysis explores the progression of risk taking by investors across 2013. While many categories of risk assets are attractively priced relative to safe assets like bonds and cash, investors have followed a steady, measured progression this year in their willingness to take risk. During the first quarter, investment flows favored hybrid assets (like high-yield bonds) and yield-oriented stocks. Then, following the threat of Fed tapering, investors moved away from bond-like stocks toward blue chip stocks, principally those listed in the U.S. We believe that a logical next step for risk tolerant investors would be towards the relatively undervalued equity markets around the world. This is particularly likely since the policy uncertainty in the U.S. is likely to be renewed early next year in both the monetary and fiscal realms.

We have consequently upgraded non-U.S. equities in our asset allocation outlook, and we expect the year to date performance gap to close between the U.S. and non-U.S. equity markets, especially if equity markets overall continue to trend higher. Indeed, market performance since July (see chart above) suggests that this rotation is already underway.

Disclosure

The views expressed are as of 10/28/13, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

The Dow Jones EURO STOXX 50 is a market capitalization-weighted stock index of 50 large, blue-chip European companies operating within eurozone nations.

The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization.

Tokyo Stock Price Index, commonly known as TOPIX is an important stock market index for the Tokyo Stock Exchange in Japan, tracking all domestic companies of the exchange's First Section.

There are risks associated with fixed income investments, including credit risk, interest rate risk and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is more pronounced for longer-term securities.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2013 Columbia Management Investment Advisers, LLC. All rights reserved. 760379