For years, I have been “running around” telling my story of currency wars and the related risk to the stability of the global financial and geopolitical systems. Very little attention has been paid, and even the seemingly interested have met my arguments with a sense of pity and apparent effort not to judge a man who may not understand “that this time it is different.” Needless to say, for many the reign of the US dollar (USD) is so assuring that other items simply do not matter; but they surely do, even if only for the reason that the currency market is a closed system—for one currency to go up, another needs to move down.

The concept of countries managing their currencies to more favorable levels (mainly to enhance export competitiveness) is not a new one, and has sparked controversy and conflict (hence “currency wars”) for nearly a century. With the Chinese renminbi being a common subject of such discussion these days, we have to recognize that not only do most market observers seem to be inept in their judgment of what really is occurring (e.g., labeling recent market moves as “devaluation”), but also that the U.S. is kind of getting what prominent U.S. Senators have been asking for: a Chinese government allowing their domestic currency to float more freely, and—possibly related—a reduction of the “stockpile” of dollar reserves accumulated over the years.

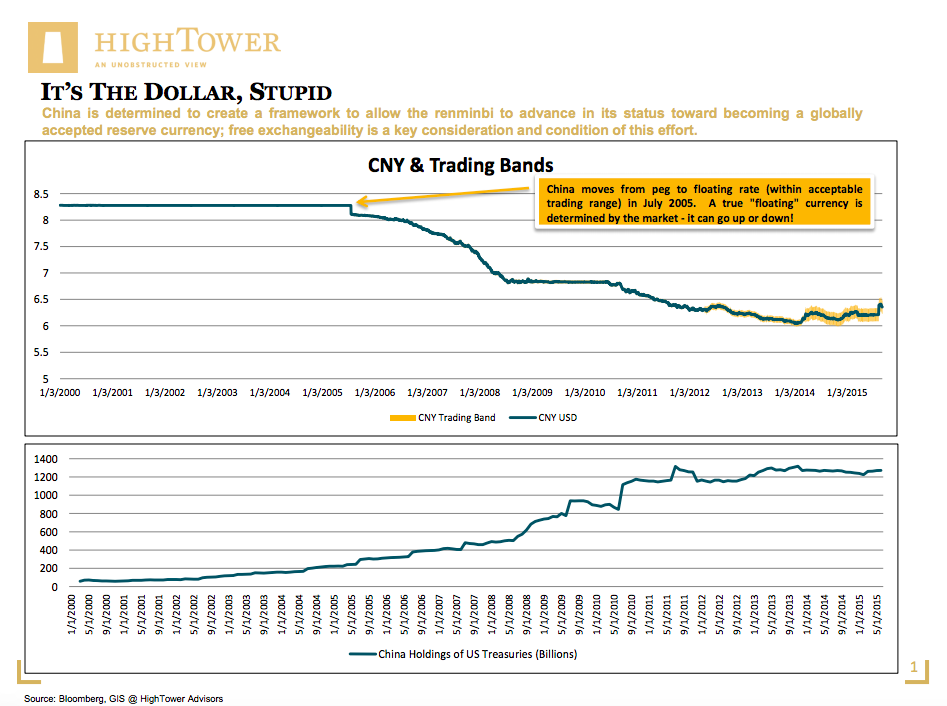

Recent and abrupt changes to the cross-rate of the renminbi vs. the USD are not considered devaluations in my book (pretty much every news outlet gets this wrong), as devaluations can only take place in a fixed exchange-rate system. Already in 2005, China made the decision to end the peg to the U.S. dollar (giving up the “fix”), and allowed the renminbi to float more freely against a basket of international currencies. With this decision, characteristically typical for a nation anchored in multi-year planning efforts, the Chinese also made it clear that the band would widen over time. What policymakers in the U.S. did not account for is that a “free” currency may not have to go up (as desired vs. the USD), but could trade down instead.

Market observers in other developing (emerging) countries may not care as much about current renminbi volatility, especially when viewed in the context of recent history. As a result of accommodative central bank policies following the Global Financial Crisis of 2007-2008, “indirect” currency devaluations have become more commonplace. In 2009, Brazil’s finance minister pointed to the weakness of the USD as the main cause of global economic imbalances (not the renminbi, as U.S. officials suggested), acknowledging that Brazil may have to take action to stop its currency from appreciating further. It is no coincidence that BRICS continue to define outlets to “ditch” the USD as a trade-based currency in international business transactions

Over the past years, the Fed’s aggressive policy stance has turned the USD into a prominent funding currency, and unleashed speculative flows into assets around the globe, mainly supporting emerging/international financial and non-financial assets. Considering the relative attractiveness of U.S. capital opportunities, and a domestic economy that has become less dependent on markets abroad to satisfy consumption, the prospect of a changing Fed policy continues to be a serious risk to the world. In oversimplified fashion, not only will money “come home,” but the U.S. will not produce enough dollars to supply the demands (and USD funding dependencies) outside its borders.

Whereas current developments pose a serious (but fading) risk to non-dollar denominated investments, we still have to consider the closed nature of the system: what goes up must come down, eventually. With this concept in mind, a strong(er) USD can buy more international assets on a relative basis. As I argued before, economic prosperity, based on dynamic and young societies, will still take place in emerging markets in the years to come. Investors need to stay globally diversified in their asset allocation, and take a strategic rather than tactical view. A related and equally important conclusion is that China is determined to create a framework to allow the renminbi to advance in its status toward becoming a globally accepted reserve currency; free exchangeability is a key consideration and condition of this effort. Whereas the transition may be a painful balancing act, particularly in financial markets, the resolution may give basis for a more optimal geopolitical setup and understanding among both developed and developing nations, therefore addressing the adverse effects of today's currency wars.

Matthias Paul Kuhlmey is a Partner and Head of Global Investment Solutions (GIS) at HighTower Advisors. He serves as wealth manager to High Net Worth and Ultra-High Net Worth Individuals, Family Offices, and Institutions.

{kind=link}