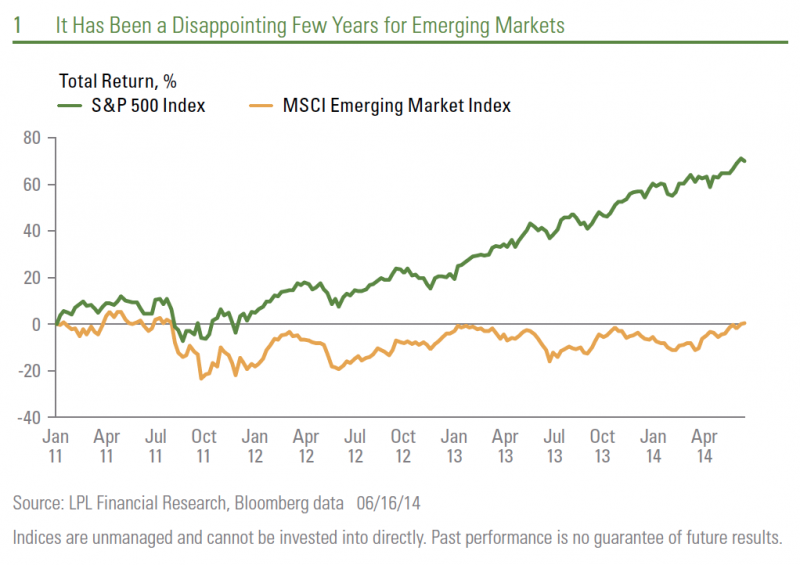

The emerging markets (EM) asset class has been especially disappointing for investors in the past few years [Figure 1], as measured by the MSCI Emerging Markets Index. However, last week EM pulled ahead of the performance of the S&P 500 Index for 2014. Might this mark the beginning of the turn for EM relative performance? We think it may. A little history may help illustrate why.

The “BRIC” Era

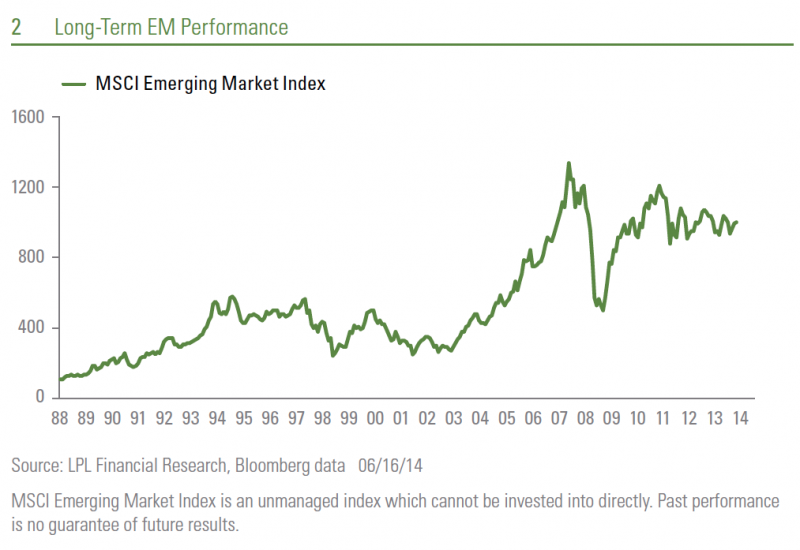

EM investors in the 1990s were used to the huge up-and-down swings of the EM asset class as EM countries in Asia and Latin America were prone to financial crises—from the Mexican “peso crisis” in 1994, to the Asian “contagion” of 1997-1998, to the Argentine debt default of 2001. But from 2002–2007, the BRIC era (named for a 2001 paper on the emerging importance of the economies of Brazil, Russia, India, and China), EM stocks experienced a decade of spectacular performance resulting from a few key drivers [Figure 2].

Growth. China’s growth surged as it entered the World Trade Organization. China’s internal growth boom drove commodity prices higher (which were further fueled by a declining dollar), which benefited commodity producing EM countries. EM economies grew faster than developed countries.

Valuation. EM valuations rose even as developed market price-to-earnings (PE) ratios fell as an environment of sluggish growth in developed economies prompted investors to seek rapidly growing EM companies. In addition to rapid growth, the valuations were supported by structural reforms undertaken in these countries that extended from the crises of the 1990s.

Interest Rates. EM countries benefitted from lower borrowing costs and an influx of foreign capital to fuel growth as global interest rates declined on lower inflation, European integration, and policymakers taking key rates to new lows.

From BRIC to SICC

From 2007 to the present, EM stocks failed to keep up with their developed market counterparts for a few reasons:

Slower growth in China. While still a remarkable 7-8%, China’s period of around 10% annual economic growth from 2002-2007 came to an end.

Improving growth in developed economies. Many emerging markets had become dependent upon developed economy weakness. The soft economy of the developed world prompted the Federal Reserve (Fed) and other central banks to pump money into the global financial system, encouraging capital to flow into the emerging markets and allowing them to run unsustainable trade and budget deficits. As global growth began to improve, the Fed has started to slow its bond purchases, and that change is prompting some emerging markets to have to quickly adjust by devaluing their currencies and sharply slowing spending.

Compression of valuations. EM stocks saw their valuations slide back to a more typical discount to the developed markets as their relative growth differential shrank and risks returned.

Curtailing stimulus. The Fed suggesting it may begin to normalize rates acted as a major headwind for EM in 2013. To demonstrate the sensitivity EM stocks have to this driver, the start of the Fed’s taper talk in May of last year contributed to a 16% decline for the MSCI EM index from May 9, 2013 to June 24, 2013. While it eventually rebounded, renewed concerns emerged in the fourth quarter and weighed again on the asset class—although to a significantly lesser degree—resulting in a loss for the year.

Turning Point

Several factors could support a turning point for the relative performance of EM stocks:

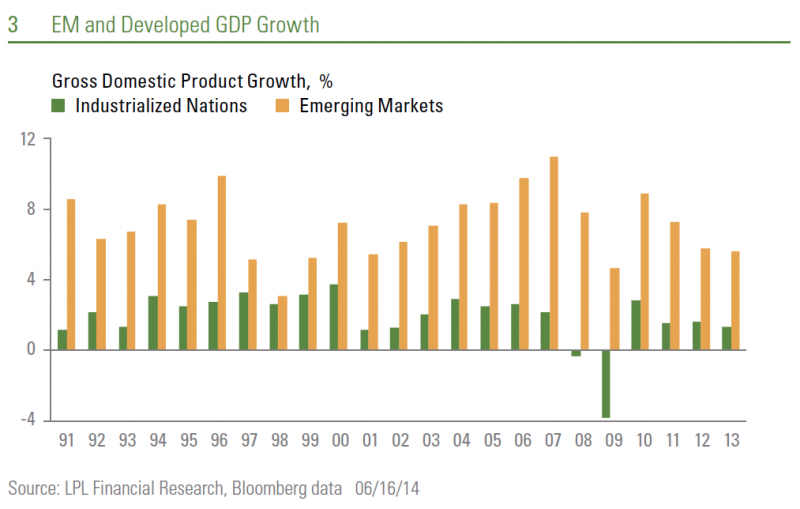

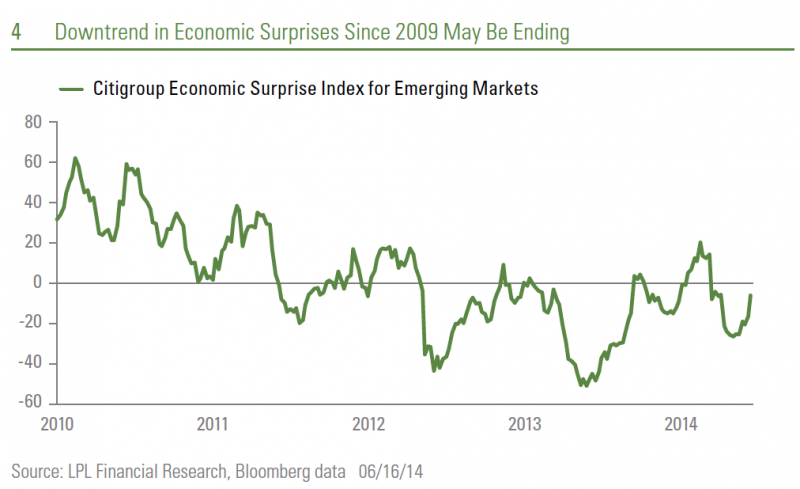

Growth. The deceleration in global growth in recent years has weighed on EM [Figure 3]. Rebounding EM economic growth appears to have been a key driver of recent outperformance with a rebound in positive economic surprises ending the multi-year downtrend in the Citigroup Economic Surprise Index for EM [Figure 4]. A driver may have been better growth in Europe, further supported by rate cuts by the European Central Bank (ECB) last week. Europe is a larger trading partner for EM than the United States or Japan, so this is a significant positive development. EM economies are highly leveraged to global trade growth, and a majority of the components of EM stock indexes are cyclical—with much larger weightings in materials and financials relative to the S&P 500 Index and significantly less exposure to the defensive health care sector.

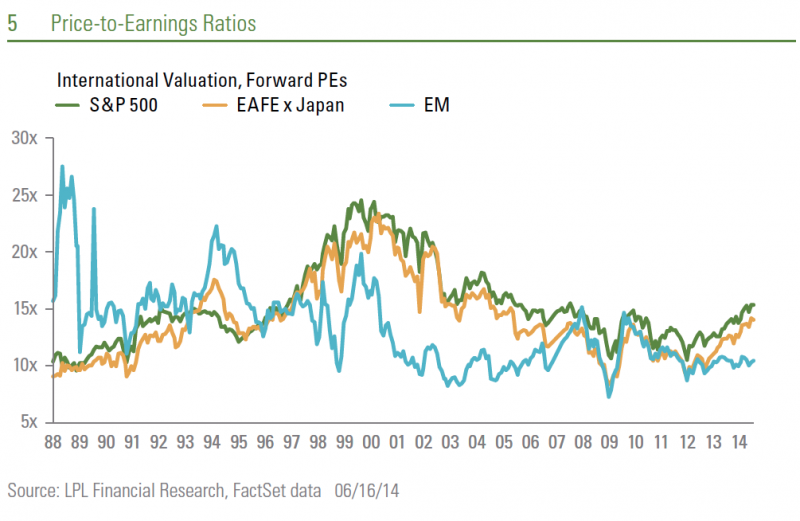

Valuations. PEs are trading at a significant discount to U.S. and other global developed stock markets [Figure 5].

Improving financial conditions. The Fed has calmed market fears over the pace of normalizing monetary policy in the United States and the ECB has cut rates, while the Bank of Japan continues to provide enormous stimulus.

Nevertheless, risks are present that could cause EM stocks to continue to lag the U.S. stock market. The biggest of these risks are China’s growth trajectory, the impact of trade and budget deficits, and political changes.

- Concerns over China’s growth trajectory have started to ease as stimulus measures began to be put in place after a very weak start to the year. But China’s “ghost cities,” rapid credit growth, and large shadow banking sector all point to the need for reforms that may slow growth.

- Broad global growth is a positive for all EMs, but trade and fiscal deficits may cause some countries to be left behind as they struggle with structural adjustments. On the other hand, rapid improvement in those vulnerabilities can drive valuations higher, as seen in Indonesia.

- Political change may stem from social unrest, conflict, and—even more importantly—a lot of elections. EM elections in 2014—including those in India, Indonesia, Brazil, South Africa, and Turkey—paint a mixed picture: some may lead to enacting protectionist policies that inflate costs while others may result in more business-friendly policies.

Despite the clear country-by-country differences, it is still relevant to consider EM at the asset class level. In general, correlations remain relatively high—and the dispersion low—across the major EM stock markets, currencies, bond yields, and economic growth rates.

After years of avoiding EM, we believe these factors, on balance, are beginning to favor the return of some portfolio exposure to EM, but only added slowly as evidence of a lasting turn in relative performance mounts.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

International and emerging market investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Forward Price-to-Earnings is a measure of the price-to-earnings ratio (PE) using forecasted earnings for the PE calculation. While the earnings used are just an estimate and are not as reliable as current earnings data, there is still benefit in estimated PE analysis. The forecasted earnings used in the formula can either be for the next 12 months or for the next full-year fiscal period.

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

Citigroup Economic Surprise Index (CESI) measures the variation in the gap between the expectations and the real economic data.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Jeffrey Kleintop is Chief Market Strategist and Executive Vice President at LPL Financial. In this role, he leads the development and articulation of LPL Financial Research market and investment strategies.