You can’t blame clients for being disappointed about the yields on fixed income portfolios. For much of the past year, 10-year Treasuries have been yielding less than 2 percent. Intermediate-term bond funds aren’t much better. The yield on iShares Core Total U.S. Bond Market ETF (Ticker: AGG)—which tracks the Barclays Aggregate benchmark—is only 2.4 percent. Where can you get richer income? Junk bonds pay more, but they can be risky. In 2008, the average high-yield fund lost 26.4 percent, according to Morningstar. (Of course, junk had a killer 2012, returning more than 15 percent.)

For many investors a better solution may be emerging markets bond funds, which yield 4.5 percent. During the 1990s, the funds delivered miserable results. But the performance has changed lately. Emerging market bonds weathered the financial crisis in relatively good shape, losing 17.6 percent in 2008. Since then the bonds have strengthened considerably.

Make no mistake, some clients may balk at the idea of shifting assets from the U.S. to Turkey or Peru. To reassure them, you can argue that there are good reasons to depend less on the developed world. While Standard & Poor’s famously downgraded U.S. debt, Uncle Sam is not the only developed country to lose an AAA rating. Other countries that have fallen from the top grade include France, Austria, and Spain. Japan slipped from AA down a notch to AA-. The developed nations have declined because their balance sheets have been deteriorating, as the governments take on huge debt burdens and economies remain sluggish.

The emerging markets present a very different picture, boasting growing economies and manageable debt levels. As a result of improving fundamentals, ratings agencies have upgraded many countries in recent years. Turkey was promoted from junk status to BBB, the lowest investment-grade rating. Other countries that have attained investment-grade ratings include Brazil, Panama, and Thailand.

Thanks to their improving credit, emerging bonds have rallied. In 2012, emerging bond funds gained 17.9 percent and ranked as the top-performing fixed-income category tracked by Morningstar. After the big gains, the bonds may no longer appear to be screaming bargains. But with balance sheets continuing to strengthen, there is good reason to believe that the funds will deliver healthy single-digit returns in the coming year.

Besides providing tempting yields and reasonable risk, emerging bonds can help to diversify portfolios. Responding to their own economic conditions and central banks, bond markets in Asia and Latin America sometimes rise when the U.S. is sinking. Consider December 2010, when yields on ten-year Treasuries spurted from 2.81 percent to 3.30 percent. For the month, the average U.S. intermediate government fund lost 1.0 percent, and long-term government funds fell 8.9 percent. But emerging markets bond funds gained 1.1 percent. The diversification benefit of emerging bonds could prove particularly valuable if U.S. rates rise in the coming year, as many economists expect.

In the past, most emerging markets bond funds focused on government issues that were denominated in dollars—not in the local currencies. Investors figured that the dollar bonds would hold their value if the local currencies collapsed. These days some funds emphasize local currency bonds, which can strengthen as emerging markets grow. Besides government bonds, many portfolio managers also hold corporate issues.

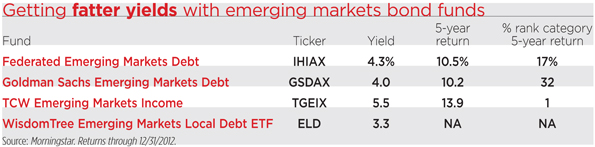

To hold a broad collection of bonds, consider TCW Emerging Markets Income (Ticker: TGEIX).During the five years through the end of 2012, the fund returned 13.9 percent annually and ranked as the top-performer in the category. Portfolio manager Dave Robbins shifts allocations, some years emphasizing dollar sovereign bonds and other times holding corporates or local currency issues. Lately he has been increasing his allocation to local currency Brazilian bonds that yield more than 9 percent. Investors demand the high yields because they worry about the country’s history of inflation. But Robbins argues that the fears are exaggerated. “Brazilian inflation rates have come down as the country’s economic policy has improved,” he says.

Another solid fund is Federated Emerging Markets Debt (Ticker: IHIAX), which returned 10.5 percent annually during the past five years. Portfolio manager Roberto Sanchez-Dahl likes BBB-rated dollar bonds in Peru and Colombia. He says that they yield around 4.5 percent, about a percentage point more than similarly rated bonds in the U.S. Sanchez-Dahl is overweight BBB-rated Mexican government issues. “Mexico has a low level of debt, and the government is showing fiscal discipline,” he says.

To hold high-quality local currency bonds, consider WisdomTree Emerging Markets Local Debt ETF (Ticker: ELD). The fund yields 3.3 percent and has an average credit quality of A. Actively managed, WisdomTree tends to underweight countries with shaky finances. “We favor countries that are running really tight ships,” says Rick Harper, WisdomTree’s head of fixed income and currency.