“True faith,” said William Ralph Inge, the one-time dean of London’s St. Paul’s Cathedral, “is belief in the reality of absolute values.” Apparently, American exchange-traded fund (ETF) investors can be counted among the faithful. Why? Because they’ve committed nearly $1.7 billion into so-called “absolute return” products.

These funds aim to consistently produce positive returns, regardless of market conditions, through non-traditional management, i.e. by employing short sales, derivatives, leverage and/or investing in unconventional assets. Rather than being benchmarked against the more common metrics such as the S&P 500 or the Barclays Capital Aggregate Bond Index, the hurdles for absolute return ETFs are typically the Consumer Price Index (CPI), the London Interbank Offered Rate (Libor) or Treasury Bills. Essentially, absolute return ETFs are publicly traded analogs of hedge funds and, as such, should exhibit relatively low volatility as well as small correlations to common benchmarks.

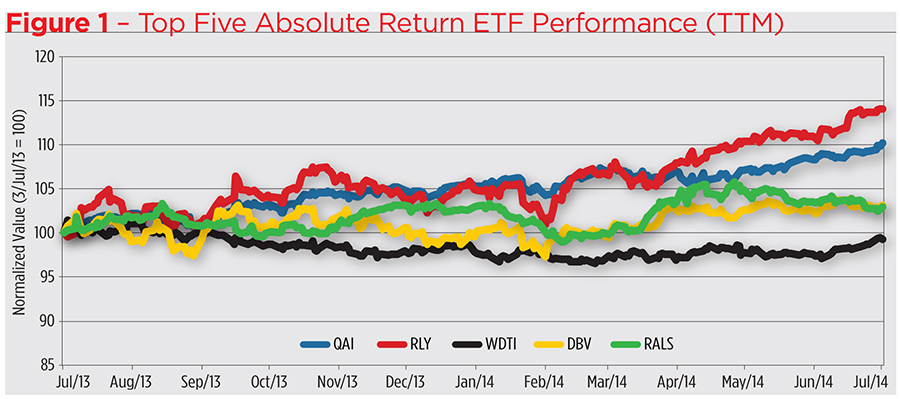

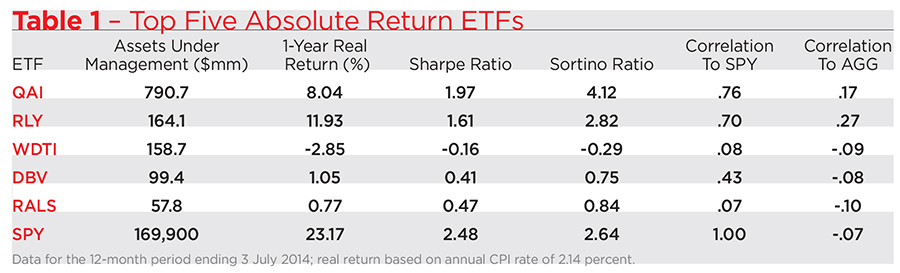

Five exchange-traded funds (ETFs) own more than three-quarters of the category’s assets. At the top of the heap, with a 48 percent market share is the IQ Hedge Multi-Strategy Tracker ETF (QAI), an ETF-of-ETFs that employs the full spectrum of hedge fund strategies, including long/short equity, market neutral, event-driven, fixed-income arbitrage, global macro and emerging markets. Despite the fund’s heavy weighting on the long side of fixed-income, its correlation to the iShares Core U.S. Aggregate Bond Index ETF (AGG), is pretty low (17 percent). QAI’s returns more closely correlate — at 76 percent — to the SPDR S&P 500 ETF (SPY), however. So it’s not exactly a hedge.

Despite the high correlation, QAI’s volatility is half that of the S&P 500 fund though the multi-strategy tracker’s Sharpe ratio is lower. Named for its creator, Nobel laureate William Sharpe, the ratio measures risk-adjusted returns as the dividend of an investment’s excess returns (the gain or loss above/below the risk-free rate) and the investment’s volatility. The higher the ratio, the better meaning a greater return per unit of risk.

Does this mean blue chip stocks are better than hedge strategies? Well, no, not necessarily. Stocks have been on a tear over the last 12 months, to be sure. But that 25 percent gain, especially in the current low-yield environment, isn’t typical. More important, though is this notion of volatility. The Sharpe ratio views the standard deviation of returns – both ups and downs — as volatility. Clearly, a string of negative returns represents “bad” volatility, but “good” volatility? That’s also considered a risk in Sharpe’s world.

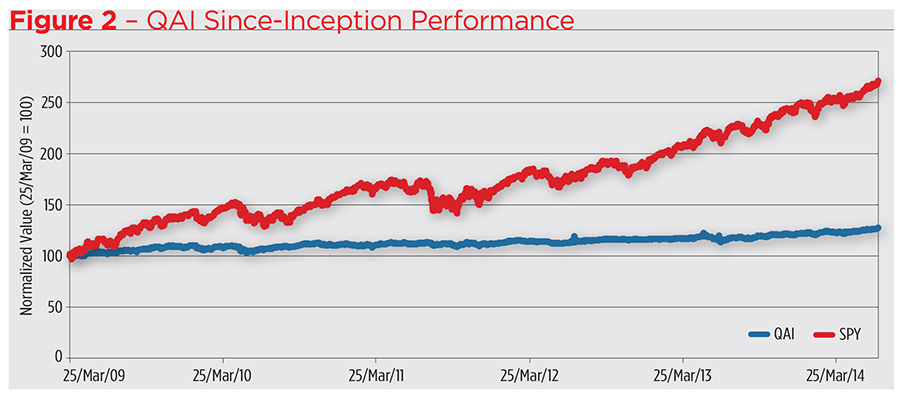

The Sortino ratio, a more recent modification of the Sharpe ratio, on the other hand, penalizes only downside volatility. When you run a Sortino comparison for QAI against the S&P fund, QAI comes out on top (like the Sharpe ratio, the larger the number, the better). The 12-month track record of QAI versus SPY (Figure 2) really paints the picture. As QAI climbed, admittedly at a slower rate than SPY, the absolute return fund experienced fewer and milder drawdowns. QAI earns a not-so-insignificant .38 beta coefficient – a measure of systematic risk with 1.00 representing the same volatility as the market’s. QAI’s alpha, or beta-adjusted excess return, comes in at .00 – not good, but not so bad, either.

And the other ETFs?

The self-avowed objective of the SPDR SSgA Multi-Asset Real Return ETF (RLY), the second-biggest product in the category, is hedging against inflation. RLY, an actively managed ETF-of-ETFs, has done that in spades. Over the past 12 months, in fact, RLY beat the CPI by nearly 12 percent. The fund’s returns were generated by a basket of a dozen commodity, real estate and natural resource ETFs. While RLY is highly correlated to equities, its Sortino ratio is slightly better than SPY’s. RLY’s 12-month beta versus SPY is .60 with a -.01 alpha coefficient.

In third place is the Wisdom Tree Managed Future Strategy Fund (WDTI), an ETF that takes its cues from the Diversified Trend Index, a momentum-based algorithm that trades currency, commodity and Treasury futures. WDTI is the only top-tier product that’s failed to beat inflation in the past year. Not surprisingly, WDTI posts a -.02 alpha coefficient on the back of a .04 beta.

The fourth slot belongs to the PowerShares DB G10 Currency Harvest (DBV). DBV was recently profiled in “The Case for Currencies." Suffice it to say that this long/short portfolio pits high- versus low-yielding currencies in emulation of a “carry trade.” DBV grosses a .32 beta and a -.05 alpha

Rounding out the top five is the ProShares RAFI Long/Short ETF (RALS), a portfolio that uses the Research Affiliates Fundamental Index approach to select component stocks on the basis of their sales revenue, dividends, book value and cash flow. RALS is the only top-tier ETF to snag positive alpha (.02) on a .04 beta over the past 12 months.

So, what’s the takeaway from all this? Well, first of all, absolute return investors are herd animals. The overlarge market share of the QAI portfolio imbues the space with the fund’s character. The 29 ETFs in the category produced 12-month real returns ranging from RLY’s 11.93 percent to the -10.89 percent cranked out by the QuantShares U.S. Market Neutral Anti-Beta ETF (BTAL). Despite the fact that more than a third of the products failed to post positive numbers, absolute return investors earned an average real return of 5.32 percent over the past 12 months on a market-weighted basis. And the cost? An average of 1.02 percent per annum.

Compare that with the 23.17 percent real return and the .09 percent expense ratio of the SPY fund and you may well ask if absolute return investors are getting what they pay for. That’s, in fact, exactly what the authors of a study published in the Winter 2013 issue of The Journal of Investing pondered. Christopher Clifford, Bradford Jordan and Timothy Brandon Riley pored over the track records of absolute return mutual funds between 2000 and 2010 and found that, despite their lower volatility, the portfolios charged higher fees and exhibited higher turnover compared to conventional stock funds. On top of that, the alternative funds failed to produce positive alpha for their investors. The researchers also found that larger absolute return funds underperformed the smaller portfolios.

We’ve seen, in the past year at least, that some of those conclusions are applicable to absolute return ETFs as well. Some, but not all. Most notably, the larger ETFs actually outperformed their smaller brethren and one at the top tier did, in fact, produce positive alpha.

There isn’t a ten-year track record for absolute return ETFs. The average ETF is only three years old. The granddaddy, the DBV portfolio, is only eight years old. Launched in 2009, the weightier QAI fund is the category’s second oldest.

Hedge funds, on the other hand, are much longer in the tooth. For example, there’s a 20-year history of the Credit Suisse Multi-Strategy Hedge Fund Index (CSMSHFI) which can be laid next to that of the S&P 500 to better visualize (see Figure 3) the long-term utility of absolute return investing.

Figure 3 – Multi-Strategy Hedge Funds vs S&P 500 Total Return

Over two decades, multi-strategy funds have outperformed the S&P 500, earning an average annual return of 19.02 percent versus 16.71 percent for the blue chip index. As you can readily see, however, there were times when hedge funds lagged stocks and other times when the alternative investments shone brighter. It’s all about the volatility. Plainly, hedge fund values don’t wobble as much as stocks. Most particularly, hedge funds haven’t suffered as many drawdowns as the equity market. Witness the Sortino ratios: for the hedge fund index, it’s 1.06; for the S&P, just .17. And alpha? Over 244 months, hedge funds produced a .11 alpha coefficient. That’s a positive number, mind you.

So is this the fate of multi-strategy absolute return ETFs like QAI? We can’t say with certainty. We can say it’s possible. Perhaps Canadian author and essayist John Ralston Saul said it best: “Nothing is absolute, with the debatable exceptions of this statement and death.”

{kind=link}

{kind=link}

{kind=link}