Hiram Johnson knew what he was talking about when he said “The first casualty when war comes is the truth.” After all, the one-time California governor culminated his political career with a stint in the U.S. Senate bookended by both World Wars.

Now in the 21st century, a bloodless war has been declared on the currency front. Or so it seems to some pundits and market observers. But is this true? Are central banks indeed engaged in a race to the bottom of the currency bin? If so, what’s the implication for investors?

Just what is a currency war?

It’s nothing more than a competition among nations eager to stimulate their economies by lowering the exchange rates for their respective currencies. Devaluation is a crutch for a state suffering from high unemployment or in pursuit of export-led growth. As the price of a currency falls, the issuer country’s exports become cheaper while imports become more expensive. That can boost employment as demand for domestically produced goods increases. Devaluation is an alternative solution to unemployment when other forms of stimulus, e.g., a boost in public spending, are unpalatable.

There are inherent dangers in systematic devaluation. First, citizens’ purchasing power can be crimped when they attempt to buy imports or travel abroad. Ultimately, that adds inflationary pressure. Another risk is retaliation by other countries. As nations try to ship unemployment overseas, international trade can be choked off.

States, through their central banks, can systematically devalue their currencies with a mix of policy tools including direct intervention in the forex market, lowering base interest rates, the imposition of capital controls and, perhaps most famously, quantitative easing.

Are we in one?

A true currencywar is a really roll-up affair. An individual country’s devaluation must, of necessity, involve a corresponding rise in other currencies. Normally, non-devaluing nations countenance small increases in their exchange rates, but may find gains intolerable in dire economic circumstances such as recessions. When a small number of states begin devaluing competitively, other countries may be compelled to join the fray to protect their export positions.

Is that where we are now? In a word, no.

Currency values are always relative, most commonly expressed as dyads or pairs, e.g, euro/dollar (EUR/USD) or sterling/yen (GBP/JPY). Comparing multiple currency pairs is a clumsy way to detect systematic devaluation. A better method is to set each currency against a common benchmark, namely gold. Pricing gold in each currency allows for easy side-by-side trend detection. A rise in the gold price is indicative of currency devaluation; a decline denotes strengthening.

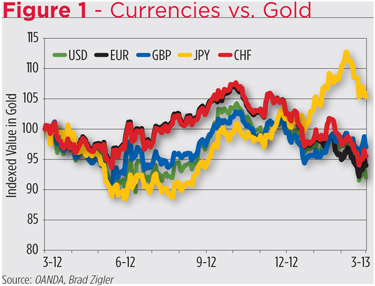

Take a look at Figure 1 which plots the value of gold across five reserve currencies -- the U.S. dollar (USD), the euro (EUR), the pound sterling (GBP), the Japanese yen and the Swiss franc (CHF) -- over the past year.

As you can see, all five currencies tracked more or less the same trajectory until January 2013. Then the Japanese yen diverged and began to cheapen, meaning it took more and more currency to purchase an ounce of gold. In the span of a month, in fact, the yen price of gold rose seven percent. The other currencies, meantime, strengthened. In other words, the price of gold dropped in terms of dollars, euro, sterling and francs. The euro for example appreciated by three percent.

What precipitated this?

Simply put, Japan's central bank signaled its willingness to pursue quantitative easing, via an open-ended bond buying program, to combat the country’s long-term deflationary recession. Despite government assertions, however, the market attributed devaluation as the scheme’s objective. No matter. The truth is that the yen’s been weakening while other reserve currencies have strengthened.

Not much of war, really. More like a skirmish.

The investor armory

If the prospect of open-ended easing emboldens investors to try to directly capitalize on a further slide in the yen, they have few options apart from the foreign exchange market or futures. For now they’ll have to trade through U.S. dollars rather than gold (more on this later). That adds some risk but the greenback’s been the best bet against gold among the reserve currencies over the past year (see Table 1).

For those who can’t abide margin trades, ProShares UltraShort Yen (NYSE Arca:YCS) is the only extant option for playing the USD/JPY cross from the short side. YCS is a passive fund that aims to provide twice the inverse daily performance of the Japanese yen priced in U.S. dollars. The fund does this through commitments in swap agreements, futures and forward contracts, as well as options. Presently, the fund’s currency exposure is obtained through over-the-counter forward contracts with two large dealing banks.

Investors considering YCS should know that the compounding of daily returns over an extended investment horizon is likely to produce a return that differs—in degree and, perhaps, direction—from a target return for the same period. Case in point: Over the first week of February, the U.S. dollar appreciated 2.8 percent against the yen, making the target for the period (remember, YCS is geared to deliver double the inverse USD/JPY return) 5.5 percent. YCS actually eased 0.6 percent then.

Returns are voluble. Over the past year the annualized standard deviation of the fund’s daily returns was 17.7 percent; the volatility for the dollar/yen cross was a relatively tame 7.1 percent. Still, with a one-year return of 29.2 percent, YCS investors can’t complain about the fund’s reward-to-risk profile. The Sharpe ratio for the ProShares product is a very decent 1.64.

The price for all this is relatively steep for an exchange-traded fund. The YCS annual expense ratio is 95 basis points (0.95 percent). Organized as a commodity pool, YCS also spits out a K-1 tax return rather than a Form 1099, meaning accounting expense for this product is higher than that of ’40 Act funds.

New weaponry?

There’s a set of currency ETFs currently in registration that includes a portfolio that prices gold in yen rather than the U.S. dollar. Once launched, the Gartman Gold/Yen ETF (anticipated as NYSE Arca: GYEN), will offer investors short exposure, versus bullion, to the Japanese currency.

Sub-advised by Treesdale Partners LLC, GYEN is not a passive product. Rather, the fund’s gold exposure will be managed in line with guidance published in newsletter editor Dennis Gartman’s eponymous daily commentary. Bethesda, Md.-based AdvisorShares Investments LLC is the fund’s advisor.

Practically, Treesdale will use the yen, obtained synthetically through the sale of currency futures or forward contracts, as the medium to finance long gold exposure through futures, forwards, swaps and other exchange-traded instruments.

Neither the fund’s expense ratio nor its anticipated launch date have been disclosed.

Though Gartman, a frequent talking head on CNBC, recently told panelists on the network’s “Fast Money” program that gold was headed higher in yen terms, he cautioned investors about gold dealings.

“It's not a safe trade," he said. "I'm always amused when people say gold is safe. Gold is not safe. Gold is a very speculative medium."

Therein lies risk. Gartman’s been caught on the wrong side of the gold trade himself. The throttling of gold exposure within GYEN will subject investors to management risk they wouldn’t have in a passive fund.

Spreading the risk

Spreading the risk

While we’re talking about managed products, investors can obtain short, albeit dilute, exposure to the yen through the PowerShares DB G-10 Currency Harvest Fund (NYSE Arca: DBV). The fund tracks the performance of a Deutsche Bank strategy than mechanically makes commitments to a half-dozen G-10 currencies at a time. Long futures positions are undertaken on the three currencies with the highest interest rates while contracts on the three currencies associated with the lowest rates are shorted. The strategy exploits the trend of higher-yielding currencies to rise in value relative to currencies with low investment rates. The fund is reconstituted quarterly and carries an 81 basis point expense ratio.

The G-10 currency universe includes positions in U.S. dollars (USD), euro (EUR), yen (JPY), Canadian dollars (CAD), Swiss francs (CHF), sterling (GBP), Australian dollars (AUD), New Zealand dollars (NZD), Norwegian krone (NOK) and Swedish krona (SEK).

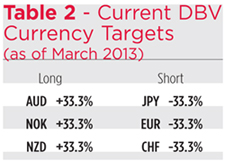

As of the last rebalancing, a third of the fund’s short exposure was yen (see Table 2).

Over the past year, DBV produced a modest 4.1 percent gain. With a volatility of 6.8 percent, the fund earned a 0.59 Sharpe ratio.

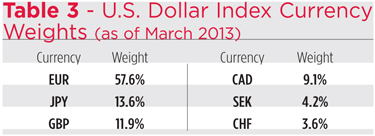

Investors inclined to ply the currency market with a passive product can get a dollop of short exposure through the PowerShares DB U.S. Dollar Bullish Fund (NYSE Arca: UUP). The fund is essentially a proxy for the U.S. Dollar Index which represents a trade-weighted basket of six currencies sold against the greenback: the euro (EUR), yen (JPY), Canadian dollars (CAD). sterling (GBP) and Swedish krona (SEK).

The index’s yen exposure, at 13.6 percent, is the second-largest after the euro (see Table 3). While the Japanese currency’s allocation within UUP is just 40 percent the size of its current share within DBV, it’s a constant presence. If Japanese interest rates rise relative to those in other G-10 nations, the short yen exposure could be dropped from DBV.

Within the past year, UUP eked out a 2.2 percent return. Volatility, at 6.3 percent, was on par with that of DBV, yielding a 0.33 Sharpe ratio.

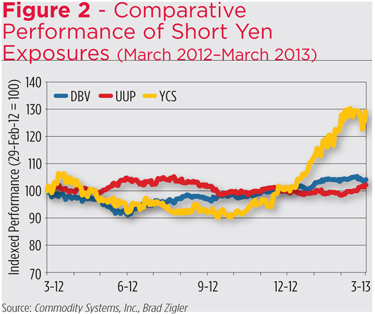

Figure 2 puts the one-year track records of three short yen exposures side by side. Just as we saw in Figure 1, the yen, here personified by the ProShares YCS fund, is a standout.

Is the yen’s weakness an opening salvo in a global currency war? Well, talk of a currency war has been just that to date, at least as far as the reserve currencies go. When you peek through the fog of punditry, the real battle line seems to be drawn around the yen. Going forward, investors should keep old Senator Johnson in mind. And perhaps General Sun-Tzu who more succinctly averred “All war is deception.”