Assets in liquid alternative funds have grown exponentially in recent years, although from a small base, as investors sought greater portfolio diversification and lower volatility in the wake of the financial crisis. But the bloom may be coming off the rose. Despite the continued hype, fewer RIAs are using alternatives in their client portfolios this year than last, according to WealthManagement.com’s 2014 AdvisorBenchmarking RIA Trend Report. Additionally, the number who say they will never recommend them grew. Some say advisors may have become disillusioned with how alternative investments perform in a bull market as investors clamor for performance over low-volatility portfolios.

“2013 was definitely a year where the S&P 500 did absolutely phenomenal, and liquid alternatives obviously lagged as they should in any extreme bull market,” said Josh Charney, alternative investments analyst at Morningstar. “But hopefully the results aren’t a product of performance-chasing, but that’s probably in the back of everyone’s mind.”

The AdvisorBenchmarking survey of about 400 RIAs analyzed the responses of advisors with client assets above $25 million—those more inclined to use alternatives. The survey found that 70 percent of advisors recommend alternatives for either many or a select few of their clients, down from 75 percent in 2013. But the percentage of advisors reporting they are unlikely to recommend alternatives increased from 17 percent in 2013 to 24 percent this year.

The AdvisorBenchmarking survey of about 400 RIAs analyzed the responses of advisors with client assets above $25 million—those more inclined to use alternatives. The survey found that 70 percent of advisors recommend alternatives for either many or a select few of their clients, down from 75 percent in 2013. But the percentage of advisors reporting they are unlikely to recommend alternatives increased from 17 percent in 2013 to 24 percent this year.

When asked what asset classes they’re considering for the next year, only 23 percent of advisors said alternatives, down from 26 percent last year. More advisors, meanwhile, are considering municipal debt for their clients, with 17 percent of respondents compared to only 11 percent last year.

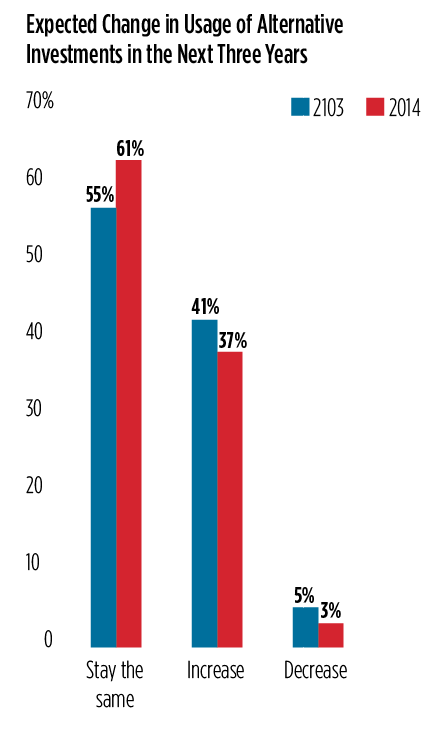

In addition, 61 percent of advisors expect their usage of alternatives to remain the same in the next three years, up from 55 percent in 2013, while 37 percent expect to increase usage, down from 41 percent last year.

“This apparent shift in advisors’ inclination to recommend alternatives may be indicative of generally lagging performance, increasingly complicated strategies, high costs, or some combination of these and other factors,” the Wealthmanagement.com report said.

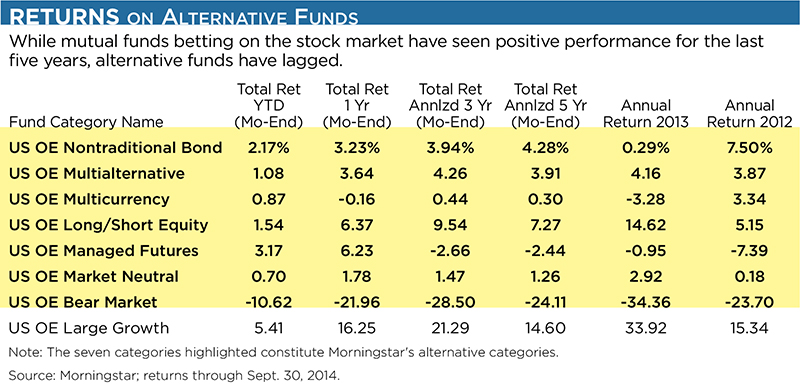

Over the last five years, alternative mutual funds have lagged the equity markets. (See chart, below.) For example, multialternative funds posted 3.9 percent in annualized returns over the last five years, according to Morningstar. Meanwhile, the S&P 500 returned about 16 percent over that period, and large-cap growth funds returned 15 percent.

But alternative funds are not supposed to beat the broader index in a bull market, Charney said. The funds offer lower beta and, ideally, less equity risk.

“The goal for a lot of them is to offer downside protection, smoother ride, better risk-adjusted returns,” he said.

The top reasons advisors use alternatives continue to be portfolio diversification, volatility reduction and risk management, the survey found.

“I think the dampening of enthusiasm is really that they were kind of sold to do everything, and they’re kind of not fulfilling some of that prophecy,” Charney said.

But the waning interest in alternatives runs contrary to fund flows. In 2012, net inflows to alternative mutual fund categories were $20 billion, compared to about $95 billion in inflows in 2013. “After record inflows into alternatives in recent years, growth in alternatives may start to ease, especially for advisors,” according to a recent survey by Morningstar and Barron’s.

Advisors may not be using the appropriate benchmarks to measure these funds’ performance. Standard benchmarks, such as the S&P 500 Index, are most commonly used to compare alternative investments, according to the Morningstar/Barron’s survey. Only 16 percent of advisors said they use custom benchmarks or model portfolios to measure alternative investments performance.

Advisors may not be using the appropriate benchmarks to measure these funds’ performance. Standard benchmarks, such as the S&P 500 Index, are most commonly used to compare alternative investments, according to the Morningstar/Barron’s survey. Only 16 percent of advisors said they use custom benchmarks or model portfolios to measure alternative investments performance.

“A lot of people still use the S&P 500 and standard indicies, which almost makes me think that maybe people are looking at these incorrectly,” Charney said. “So maybe they do have sort of a false perception of how these are supposed to return.”

Many RIAs—even those with $1 billion or more in assets—have only one research person for the entire firm, so they may not have the time and resources to conduct the due diligence necessary on alternative investments, said Dan Thibeault, president and chief investment officer of GL Capital, which recently launched a liquid alternatives database. In contrast, the wirehouse firms and other b/ds have large research teams vetting these investments.

“In the RIA world, they seem to be spending the most amount of time, but there’s not a lot of volume to show for it because they’re taking their time and trying to get a small feel for it early on,” Thibeault said.