Less than two years ago, July 2016 to be precise, 10-year Treasury notes provided a parsimonious yield of 1.37 percent. At the same time, 2-year notes were enticing with 58 basis points, which at the very least was more attractive than the 14 basis points you could have gotten in 2011. I put this out there for context against the brouhaha over the 10-year hitting 3 percent—the first time they’ve done that in over four years, which has been spotlighted by just about every reporter and related headline I’ve seen over the last several days. Is 3 percent more important than any other level or the 18-fold rise in 2-year notes?

Of course not. Yields have been in a bear market for rather a long time now, though a grudging one, judging by its protracted trajectory, though I’ll grant the nearly 100 basis point gains in 10 years since 2.05 percent as recently as September is rather stellar. Three percent is a psychological number, a benchmark, a nice round figure, but other than for a sporadic confluence of chart patterns is merely that. The headlines generated hinting that a breach of 3 percent is tantamount to a dam-busting that can only mean dramatically higher yields is, I think, more about a slow news day when it comes to interest rate influences.

The bottom lines are: (1) the Fed is hiking, (2) with a more hawkish tone adding to that, (3) it remains late April when seasonals are still bearish, (4) we’re about to see another increase in Treasury issuance which is merely the tip of the deficit iceberg, (5) oil and commodities aren’t helping the bond bulls, (6) the dollar is also worried about the deficit, and (7) if I were an investor I’d be sitting on my bond hands even as I start to drool over yields and their consequences for risk assets.

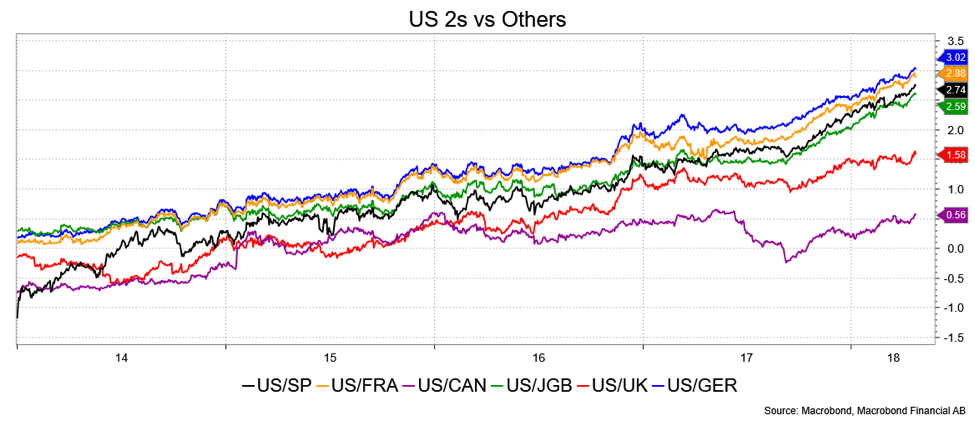

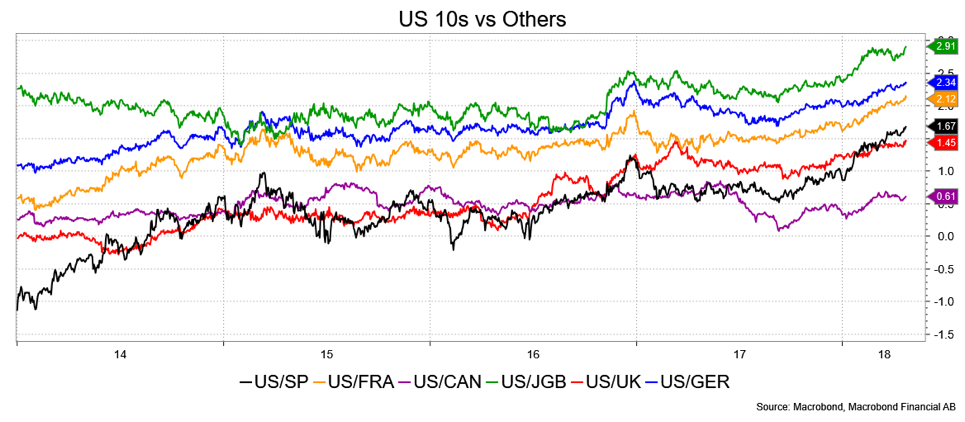

But let me get back to basics. First, yields are up and seem to be starting to worry stocks or, at least, with the drama elucidated by the mere printing of 3 percent 10-year notes (to say nothing of 2.50 percent 2-years—the most they’ve offered since 2008—or 2.85 percent 5-years). Second, there’s the seasonal pattern to consider (more in due course). Third, rate differentials surely must look compelling. Fourth, I continue to think rates can edge higher for all the right reasons, but don’t see the compulsion to move beyond my hopeful 3.25 percent to 3.5 percent target.

Have you noticed the rate differentials? The U.S. is at multiyear highs vs. everyone and the dollar, well, is cheaper too. With no insight other than experience and longevity, I suspect that there’s targeted buying interest and that’s where benchmark yields may come into play. I refer to 3 percent 10-years or 3.25 percent 10-years, which makes the upcoming “refunding” especially interesting.

This surely helped inspire a “Tail Risk” note in the Financial Times, which teased with the header “Treasury yields ‘attractive’ as inflation risk dims.” The upshot was the mention of several investors, Pimco, Fidelity and BNP by name, who are looking at current yields and liking them. The view was that inflation could put some upward pressure on rates short term, but maintained it was really only a gradual gain, and the bad news, as well as the Fed, is well priced in. Maybe I should adjust my 3.25 percent to 3.5 percent 10-year target?

Oh, the headline—The 3 Percent Solution?—refers to the Sherlock Holmes’ story The Sign of Four, where it was revealed that Holmes was a cocaine user, utilizing a 7 percent solution. When asked by Dr. Watson what he was doing Holmes said, “It is cocaine,” he said, “a seven-per-cent solution. Would you care to try it?” Holmes used cocaine when he wasn’t on the case, bored in other words, and so did it to stimulate his cerebral cortex.

Thus, in my convoluted way, I offer up the 3 percent to a bond market in need of stimulus at the moment, waiting on new data, inputs or tweets on everything from trade to North Korea and to decide for itself what the curve’s action is really telling it.

(NB: Cocaine was, at the time, considered a wonder drug—perhaps like bitcoin in more modern times—but was eventually condemned, made illegal, and deemed an “evil” by Holmes in later works.)

David Ader is Chief Macro Strategist for Informa Financial Intelligence.