By Eric Balchunas

(Bloomberg View) --The latest misdirected attack on exchange-traded funds centers on the assumption that they haven’t been tested in times of severe market stress. The issue has taken on more relevance as many brace for a correction in equities with the long bull run leaving valuations stretched.This is yet another claim that can easily be refuted with some data, but I get why the myth exists. ETFs have gotten a lot of media coverage lately, so they probably seem new to many people. But they’ve been around for 25 years.

Since then, there’s been some $210 trillion of ETF shares traded, according to the New York Stock Exchange. With an estimated average trade size of about $22,000, that breaks down to just under 10 billion individual trades. In terms of customers served, those are McDonald's-level numbers. ETFs have survived the bursting of the internet bubble, Sept. 11, 2001, the worst financial crisis since the Great Depression, flash crashes, the Federal Reserve-induced "Taper Tantrum" of 2013, the U.K.'s "Brexit," Donald Trump's surprise presidential election win, and all sorts of minor market spasms and exchange glitches. The structure is durable.

To be sure, there have been some hiccups, namely the first hour of trading on Aug. 24 when stock trading halts forced ETFs to trade at discounts because of in a so-called market plumbing issue that has been resolved. Even so, only about 3 percent of the $240 billion of ETF volume had issues. So, historically, we are looking at maybe 30,000 trades that had known issues out of 10 billion!

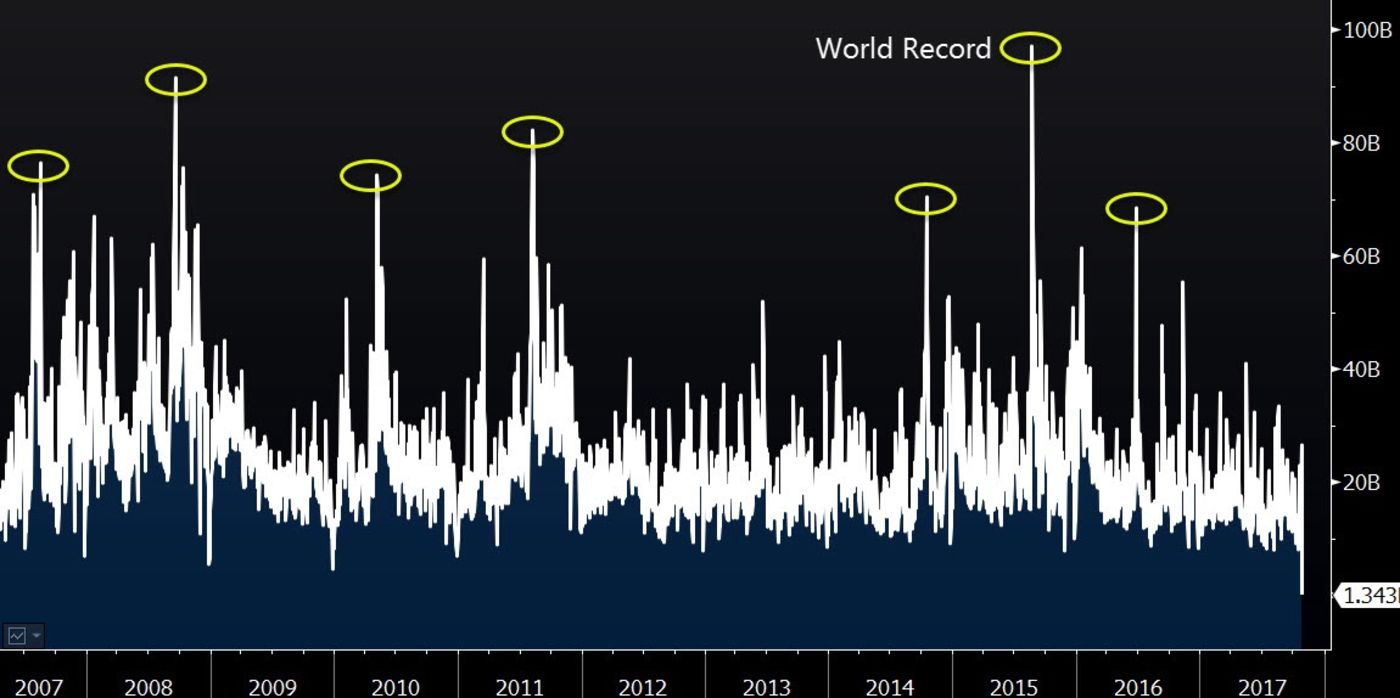

That's not to say ETFs are perfect or there won't be issues in the future, but in general investors have had a good experience. In fact, the more the attacks escalate, the faster the flows seem to come in because money tends to flow to where it is treated best. The $254 billion SPDR S&P 500 ETF Trust, known by its ticker symbol of "SPY," is a good example. The ETF usually sees about $17 billion of its shares traded daily, but that can rise substantially on active days. Volume reached $98 billion on Aug. 24, a record for any equity. It has also traded more than $60 billion during some of the worst days of 2008. By comparison, an average of about $3 billion shares of Apple change hands each day.

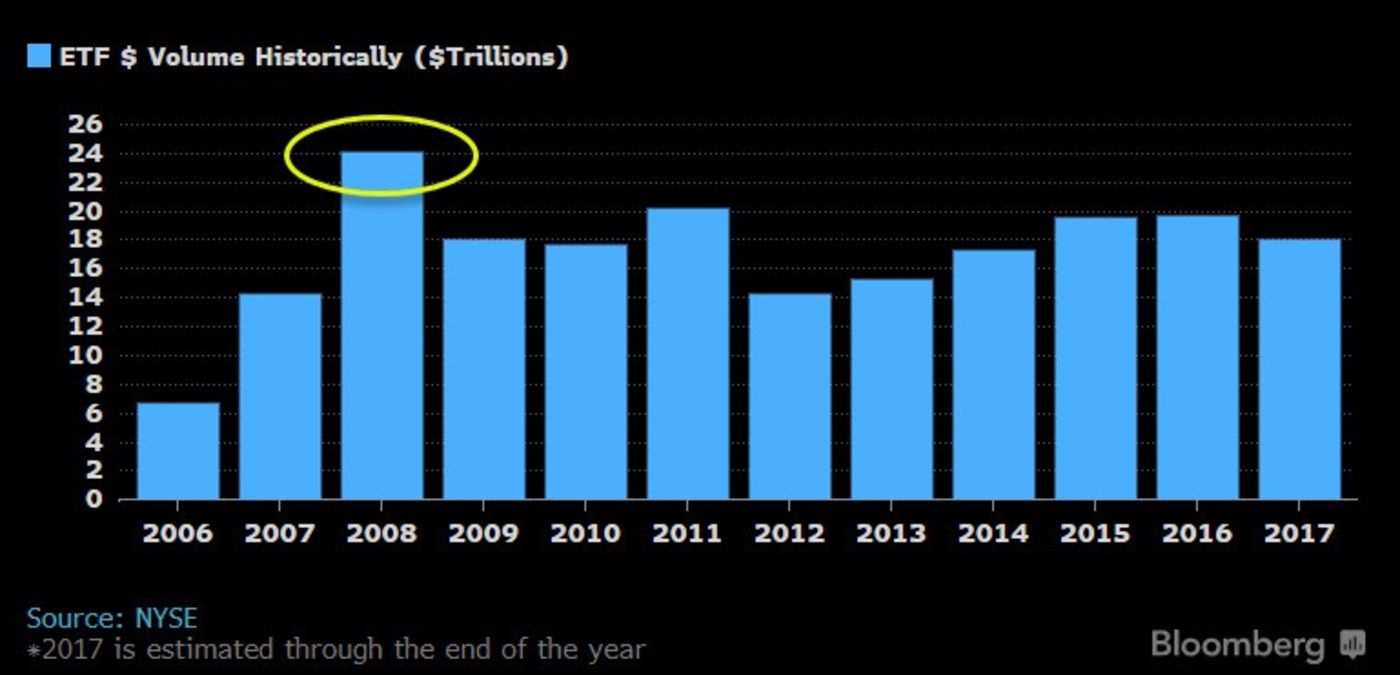

SPY is emblematic of all ETFs in that trading is most active when markets crack. That is why 2008 still remains the biggest year in terms of volume for ETFs, even though ETFs only had a third of the assets they have now. Their performance during the stresses of 2008 is a big reason many investors -- including some of the most sophisticated institutions -- either began or ramped up their usage of ETFs. In fact, SPY took in $39 billion in new cash in 2008 -- a record for flows that still stands.What is also notable is that about 90 percent to 95 percent of ETF volume is just the ETF shares themselves and doesn’t involves the underlying securities via creation and redemption activity. In other words, they provide a liquidity buffer for stocks, which is why the U.S. Securities and Exchange Commission suggested they be created back in 1988 as a solution to what went wrong in the crash of 1987.

No doubt ETFs will experience a bad day just like any other investment vehicle, but the notion that ETF investors will be stuck when the rest of the market is trading is false based on the data. There will be times when markets are in a sort of paralysis and nothing is trading, but that's not specific to ETFs. Bad days are bad for everyone.This brings us to more important questions: Are ETF investors ready to be tested? Are long-term investors who use ETFs for their low cost and tax efficiency prepared for a sell-off and properly diversified? Will they sell out of an ETF just because they can? Lack of discipline can wipe out the cost savings provided by an ETF and then some. Learning and practicing the art of doing nothing is the next leg of this investor enlightenment era -- the current being controlling costs.The media doesn’t help things by tending to refer to a potential selloff as some kind of disaster instead of simply part of a normal cycle. There’s nothing wrong with a sell-off, especially for long-term investors. Selloffs are part of life like flat tires or getting a cold. It isn't a one-way street. And even if the S&P 500 dropped 20 percent next three months, it would still be up 73 percent in past five years!ETFs are ready for the next storm, but are investors?

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Eric Balchunas is an analyst at Bloomberg Intelligence focused on exchange-traded funds.

To contact the author of this story: Eric Balchunas at [email protected] To contact the editor responsible for this story: Robert Burgess at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view