Remember your first car? You probably had some good times in it –passing your driver’s license exam, going to the prom, driving to your first job. You most likely have a different car now that you’re older – one more suited to your current lifestyle and needs. I’ll bet your current car is a lot safer and more reliable than that first one. A car is a motor vehicle you use to reach your destination. Like a car, an investment portfolio is a vehicle you use to reach your clients investment goals.

My first vehicle was a 1962 Land Rover. I bought it when I was a teenager for a few thousand dollars. It was a faded green safari vehicle with a spare tire on the hood, a crank starter handle which extended through the front bumper to get the straight-4 engine going even with a dead battery, and removable doors and top for open air summer driving. The Rover looked like it had just driven out of the Serengeti plains. With its heavy-duty leaf springs, it wasn’t the most comfortable vehicle, but I could usually count on it to get me where I was going. It wasn’t really a “Sport Utility Vehicle” –rather it was just a utility vehicle. The Rover was not very fast; I could get it going comfortably around 55MPH on the highway, nor was it comfortable, but it was generally fairly reliable.

My first vehicle was a 1962 Land Rover. I bought it when I was a teenager for a few thousand dollars. It was a faded green safari vehicle with a spare tire on the hood, a crank starter handle which extended through the front bumper to get the straight-4 engine going even with a dead battery, and removable doors and top for open air summer driving. The Rover looked like it had just driven out of the Serengeti plains. With its heavy-duty leaf springs, it wasn’t the most comfortable vehicle, but I could usually count on it to get me where I was going. It wasn’t really a “Sport Utility Vehicle” –rather it was just a utility vehicle. The Rover was not very fast; I could get it going comfortably around 55MPH on the highway, nor was it comfortable, but it was generally fairly reliable.

Later in life I drove a sports car. It was a 2-seat convertible with a 390 horsepower V8 engine. It had a formula one style transmission, with steering wheel mounted shifter paddles. That car was fun to drive, and fast. The problems I had with the sports car, though, led me to realize that it really wasn’t the right vehicle for me. The low-profile tires tended to develop frequent sidewall failures – golf-ball sized blisters would pop out of the tires whenever I drove over any kind of pothole in the street. Replacing those tires got expensive. Also, the sports car was pretty useless in the winter – with more than several inches of snowfall it would literally bottom out in the snow and require a tow. Normal maintenance charges were orders of magnitude more expensive due to the costly Italian parts. One day the automatic top stopped working for some mysterious reason and back it went to the shop. While the car was comfortable and fast, it turned out to be an impractical vehicle for getting me to my destinations on a consistent basis.

Your clients have goals that they want – in many cases, need – to achieve; often for lifestyle planning in their retirement years. There are a wide variety of investment styles and strategies to choose from.

Some managers take the “utility vehicle” approach to investing. They aim to perform like a market index, and their portfolios can grow over time, but because these portfolios can have market-like volatility and costly drawdowns, it may take longer than clients expect to reach their investment goals. This approach has been sometimes referred to as “closet indexing”. It can be an uncomfortable ride for investors with real-world investment goals.

Other managers take the “sports car” approach to investing. Their portfolios take higher risks and appear to do well in strong market environments –yet in choppy and declining markets they can lose even more value than the markets do. Sometimes this is caused by hidden or unnecessary risk exposures in the portfolio, and it seems to be a common characteristic of an exclusive focus on growth oriented stocks. Such severe losses of capital are extremely difficult to regain, with or without active management.

Both the utility vehicle approach (closet indexing) and the sports car style of investing (high risk growth) can cause a portfolio of securities to perform well during strong bull markets, such as the one we are enjoying today and the one back in 1999-2000. In the later stages of a bull market, we often witness growth-oriented stocks outperforming stocks with reasonable valuations. In the third quarter of 2013, growth stocks achieved nearly double the return of value stocks. The problem is that they both can lead to unacceptable losses of capital in less benign times, such as the market correction back in 2001-2002.

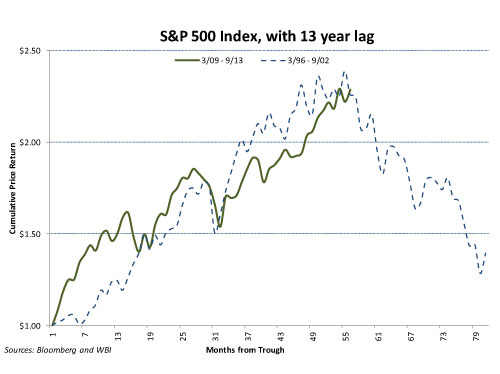

Is it possible that we are in the final innings of the current bull market? The chart below compares the current stock market as represented by the S&P 500 Index with the stock market expansion and retraction 13 years ago. The current market has been rising for four and a half years since its last major correction in March 2009. The growth path of the current bull market is remarkably similar to the growth of the market during the “dot com bubble” from 1996 through 2000. In the chart below the solid line shows the current market through the end of the third quarter 2013, and the dashed line shows the rise and fall of the dot com bubble which began its implosion in September 2000.

For example, $1.00 invested in the S&P 500 Index at the market trough at the beginning of March 2009 would have grown to $2.29 – more than doubling in value – by the end of September 2013. This is very similar to the growth of the S&P 500 Index thirteen years earlier during the dot com bubble. From the beginning of March 1996 through the end of September 2000, $1.00 invested would have grown to $2.26 after peaking the prior month at $2.39 – nearly identical growth to the current period, with similar levels of volatility. While we do not imagine that the performance of the market in a previous period could forecast its movements more than a decade later, it is nonetheless instructive to look at the subsequent decline in the dashed line. Over the following two year period, growth stocks led the market lower – the S&P 500 Index retreated from the peak of $2.39, destroying capital and leaving our hypothetical investment languishing at $1.28 by the end of September 2002.

We prefer well designed, carefully implemented, “safety first” approach to investing. For me, this is the right investment philosophy and approach. I believe it is the morally right thing to do as a fiduciary entrusted with client assets to manage. I believe it is our duty to guard investment capital. We employ a value-oriented approach to security selection and a systematic approach to active risk management. Our focus on dividend-paying stocks is intended to provide an additional margin of safety and to buffer the portfolio from the effects of inflation and market downturns. By focusing on finding value, we seek to identify securities with a higher likelihood of purchase at low prices and sale at high prices. In contrast, growth-oriented approaches attempt to “buy high and sell higher”, often with no dividend protection – a recipe for investment disaster in my opinion. It is important to mitigate the many behavioral biases that can damage investment results. Irrational decisions made in the face of incomplete information, emotional responses, uneven responses to reward and risk, hindsight bias, and overconfidence are problems across the investment landscape, especially when the investment process is highly subjective. In contrast, we designed a rational, systematic approach that is intended to avoid these issues to the extent possible.

Currently I drive a Jeep. It combines all the reliability and dependability benefits of the old Rover with comfort and performance closer to the sports car – but without either car’s issues. It is a safe vehicle. It is a reliable vehicle. It’s the best of both worlds. It gets me where I want to go, consistently and comfortably.

In 2014-2015, could we experience a decline such as the one that occurred in 2001-2002? Only time will tell. The best approach to investing is designed to get clients to their investment goal primarily by attempting to avoid permanent and unacceptable losses of capital. It’s an approach designed to keep working under any conditions, capturing a healthy amount of bull market gains while seeking safer results in choppy and bear markets.

Craig French is a portfolio manager at WBI Investments and can be reached at www.wbiinvestments.com. The firm manages $2.3 billion for investment advisors and their clients in high yielding dividend paying stock portfolios.