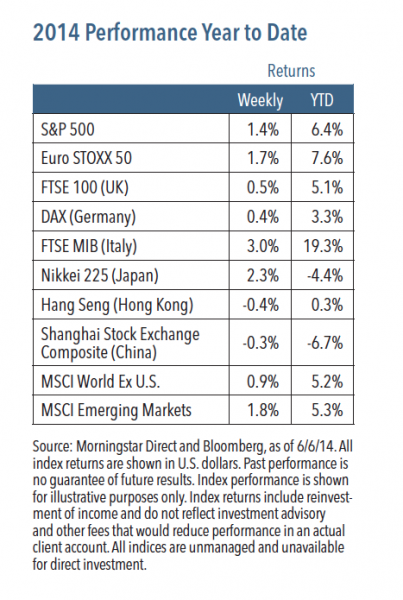

The macro backdrop last week was positive for the markets. As expected, the European Central Bank (ECB) cut interest rates, highlighting the favorable global monetary policy backdrop. Closer to home, solid vehicle sales and a good May labor market report gave investors additional reasons to bid up stock prices. The S&P 500 Index advanced 1.4 percent, (1) marking a third straight week of gains above 1 percent — the longest such streak since last September. (1) A closer look at the rally also shows that investors were in a “risk-on” mode, with small cap stocks and cyclical areas of the market outperforming. (1) Looking ahead, we believe the combination of an improving world economy, low levels of volatility and easy global monetary policy should continue to provide support for equities.

“An improving economy should lead to better corporate earnings, which should translate into higher equity prices.”

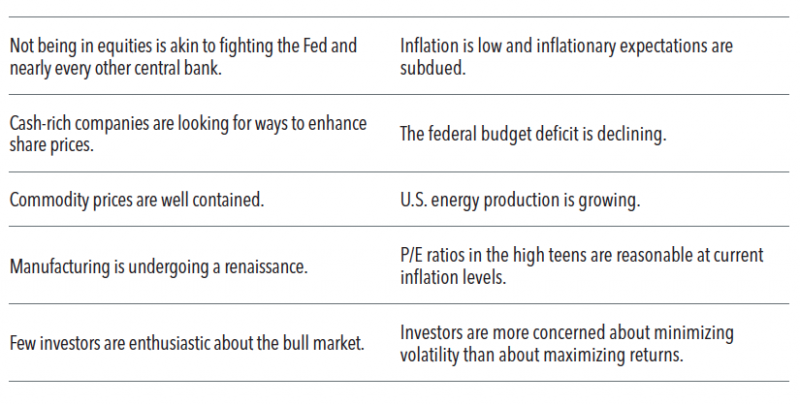

Ten Reasons to Stick with Equities

The bull market has now gone 31 months without a 10 percent correction. (1) At some point, we’re bound to see one (perhaps caused by an inflation scare), but for now, we would argue that stocks still have room to move higher. On this point, Strategas Research Partners (2) has recently been discussing reasons to remain constructive toward equities, and we think it is worth sharing some of them:

Weekly Top Themes

- Payrolls rose slightly more than expected, advancing 217,000 in May. At the same time, the unemployment rate held steady at 6.3 percent and average hourly earnings rose. (3) The data suggest the economy is growing at a moderate pace.

- The move by the ECB met market expectations. The ECB is clearly concerned about the growing threat of deflation, and we believe Europe is in need of some serious growth-oriented structural reforms.

- The Fed’s June beige book reported a moderate expansion of economic activity, with almost all districts reporting stronger consumer spending. (4)

- The trade deficit widened, adding modest downside risk to second quarter GDP growth. (5)

- With consumer price inflation hitting 2%, concerns may start brewing about whether we are in the early stages of an inflation cycle. (6)

The Big Picture: Invest for a Pro-Growth World

The current bull market has been progressing for five years, but we do believe it should persist. We also expect economic growth to continue to improve, bond yields to rise from currently low levels and the U.S. dollar to advance against most currencies in the coming months.

Altogether, such an environment argues for what we call a moderately pro-growth investment stance. Specifically, we think that an improving economy should lead to better corporate earnings, which should translate into higher equity prices over the coming six to twelve months. As such, from an asset allocation perspective, we favor equities over bonds. We also expect to see cyclical market sectors outperform defensive ones. In anticipation of rising rates, we also believe that fixed income credit sectors tend to look more attractive than developed market government bonds.

1 Source: Morningstar Direct, as of 6/6/14. 2 Source: Nuveen Asset Management and Strategas Research Partners. Used with Permission. 3 Source: Bureau of Labor Statistics http://www.bls.gov/ news.release/empsit.nr0.htm. 4 Source: U.S. Federal Reserve http://www.federalreserve.gov/monetarypolicy/beigebook/beigebook201406.htm. 5 Source: Bureau of Economic Analysis http://bea. gov/newsreleases/international/trade/tradnewsrelease.htm. 6 Source: Bureau of Labor Statistics. http://www.bls.gov/news.release/cpi.nr0.htm.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

Robert C. Doll, CFA is Chief Equity Strategist and Senior Portfolio Manager for Nuveen Asset Management. Follow @BobDollNuveen on Twitter.