By Rachel Evans

(Bloomberg) --What do you call a bond trader who doesn’t trade bonds? An ETF investor.

Yes, that’s a bad market joke. But it’s also a legitimate issue that debt specialists will be grappling with over the next decade if BlackRock Inc.’s forecast for a seismic shift away from trading individual securities comes true.

The growth in instruments tied to an index -- such as derivatives or exchange-traded funds --- will outpace any gains for bonds, with trading in debt ETFs set to double over the next five years to $15 billion per day, according to strategists at the world’s largest money manager. And with liquidity increasingly following the money into passive strategies, bond traders may have to adapt or perish.

“What has changed is the way that people actually trade,” BlackRock’s head of trading, Richie Prager, said during an interview in New York. “Look what happened in the equity market with all the different equity indices that have been created. Think about applying that to the bond market.”

In Prager’s vision of the future, bond dealers no longer focus on individual securities. Instead they command a dashboard of bonds, credit-default swap indexes, total return swaps, ETFs and derivatives on those ETFs, while their peers across the desk weigh the relative value of these same possible structures. With BlackRock being the largest issuer of ETFs in the U.S. and Europe, the asset-management giant has a substantial stake in seeing this come to pass.

Crisis Consequence

It’s all a long way from when Prager started trading bonds more than three decades ago. Even when the financial crisis hit in 2008, buying and selling debt was an over-the-counter business, driven by dealers taking on risk for a price they negotiated over the phone.

But the wave of regulation that followed the credit crunch ended all that, shrinking banks’ balance sheets and inventories of individual bonds. In the investment-grade bond market, traded volume as a proportion of outstanding bonds has slumped from more than 100 percent to about 65 percent since 2005, according to MarketAxess data quoted in a new report by BlackRock. Meanwhile, the cost of doing deals has jumped, the money manager wrote.

“ETFs have filled that void,” according to Larry Whistler, chief investment officer at Nottingham Advisors and a former bond trader for Merrill Lynch. “We’re able to trade, just in a little bit different fashion, via the ETF versus the individual security,” Whistler said by phone from Buffalo, New York, where he helps oversee more than $1.1 billion using both bonds and ETFs.

Average daily trading in BlackRock’s largest investment-grade corporate debt fund, LQD, has grown to $526 million this year, while total return swaps on the underlying index have risen to $38 million over the same period. That’s still far below the $17.5 billion of daily turnover in individual securities, but the alternatives are growing more rapidly, according to BlackRock’s report.

Skeptical Eye

Still, some aren’t convinced that ETFs are the answer, either because they see more opportunities away from benchmarking or are uncertain about whether passive products like most ETFs will work during difficult periods. And others, like Gene Tannuzzo, who manages three funds including an ETF for Columbia Threadneedle Investments, just don’t like paying fees to a rival.

“We’re more likely to use a little bit of CDX than to use an ETF,” he said of CDS indexes. “You can justify it either way, but where we’ve come down is it’s a little bit harder to justify having a separate asset manager’s name in your portfolio.”

BlackRock’s unfazed by all of this.

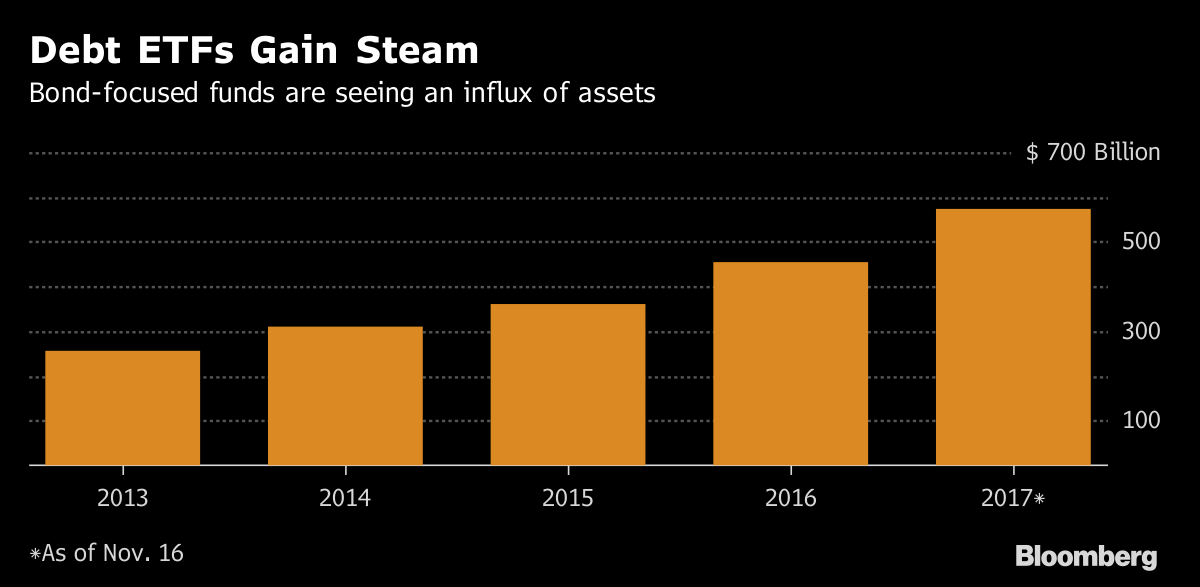

The firm already manages $284 billion in debt ETFs, almost half the U.S. market, and expects the asset class to grow to $1.5 trillion globally over the next five years. Trading doesn’t beget inflows, and vice versa, but the two are highly correlated. To BlackRock, capturing a substantial part of that growth is the key to the future.

Investors that want to trade “will gravitate to the venue and the format where it’s most efficiently priced to trade,” said Steve Laipply, head of fixed-income strategy for BlackRock’s U.S. ETF business. “That could be in single security form, it could be in derivative form, it could be in ETF form. We see the fluidity between those venues increasing over time.”

To contact the reporter on this story: Rachel Evans in New York at [email protected] To contact the editors responsible for this story: Nikolaj Gammeltoft at [email protected] Eric J. Weiner, Kenneth Pringle