Our Most Attractive and Most Dangerous stocks for December were made available to the public at midnight on Wednesday. Our Most Attractive Stock portfolio rose 3.3% last month, outperforming the S&P 500 (+1.9%). Our Most Dangerous Stocks (+0.5%) increased by less than the S&P 500 and outperformed as a short portfolio.

Universal Insurance Holdings (UVE) was up 66% in November, making it our top-performing pick. Assured Guaranty (AGO) led the way for our large cap picks with a 14% gain. Nuverra Environmental Solutions (NES) was our best small-cap short call, declining by 27%. Electronic Arts (EA), which was featured last month and remains in the Danger Zone, dropped 15% in November.

December sees 11 new stocks on our Most Attractive list and 12 new stocks fall into the Most Dangerous category.

Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

Most Attractive Stock Feature For December: LF

LeapFrog Enterprises (LF) is one of the new additions to the Most Attractive list this month. LF’s stock price declined by 3% over the past month, which made it cheap enough to make the Most Attractive list.

LF sells educational entertainment products for children, most notably the LeapPad family of children’s tablets. Parents arespending more money than ever on technology devices for their children, and LF has benefited greatly from this surge in demand. In both 2011 and 2012 LF increased its after-tax profit (NOPAT) by roughly 200%.

LF is not going to continue to grow profits by 200% a year, but healthy growth in the near term appears likely. Larger companies such as Samsung (SSNLF) have begun to enter the children’s tablet market, but LeapPad tablets remain the highest rated across most consumer review sites.

Another good sign for LF is that it’s growth in the past two years has come organically. Rather than increasing invested capital to fuel growth (like our Most Dangerous stock below) LF has achieved growth through margin expansion and increasedROIC. From 2010 to 2012, LF’s NOPAT margin increased from 2% to 11%, and its ROIC increased from 2% to 23%. Growing revenues at a large clip while also expanding margins means you have a good product and a well-run business.

Since LF has not been increasing its invested capital, the company has been accumulating cash. As of September 30 the company had nearly $80 million (14% of its market cap) in cash and equivalents, a number that should increase after the Christmas season revenues have come in and inventories have thinned. This excess cash gives LF the resources to expand its lineup of products, more aggressively market its existing products, or simply return cash to shareholders.

Despite LF’s recent growth, the stock remains cheaply valued. At its current valuation of ~$8/share, LF has a price to economic book value ratio of only 0.9, which implies a permanent 10% decline in NOPAT. In the past I’ve warned investors against small companies in fast growing industries in the past, but those were all valued for massive growth. Even if larger companies manage to take some of LF’s market share, it seems unlikely that its profits would permanently decline. LF looks like a good bet to beat the market’s modest expectations.

An acquisition by a large toymaker such as Mattel (MAT) or Hasbro (HAS) is also a possibility, especially as LF CEO John Barbour has publicly stated the company is open to the idea of an acquisition. Even if it doesn’t get bought out, LF’s cheap valuation and strong growth prospects make it one of our Most Attractive stocks.

Most Dangerous Stock Feature For December: ECL

Ecolab Inc. (ECL) is one of the new additions to the Most Dangerous list this month. ECL fell onto the Most Dangerous list for December to the improvement in rank of other stocks.

ECL offers a great example of the high-low fallacy. By buying up smaller companies, ECL has increased its reported earnings per share while actually decreasing its economic earnings. The company might have an improved accounting bottom line, but it is not actually creating value for shareholders.

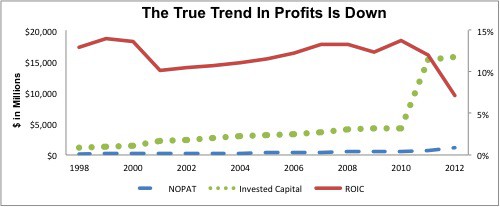

Figure 1 shows how the increase in invested capital, rather than any improvement in operating efficiency, has led to ECL’s profit growth. From 2010 to 2012, ECL’s invested capital increased 270% while NOPAT only grew by 89%. As profit growth lagged behind the expansion of the balance sheet, ECL’s ROICdeclined from 14% to 7%.

Figure 1: Invested Capital Growing Faster Than NOPAT Means ROIC Declines

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

ECL’s 7% ROIC falls below the median ROIC of 8% for the 32 specialty chemical producers we cover. Despite its apparent growth, the company is actually falling behind the competition in terms of value creation.

In addition to decreasing ROIC, ECL’s acquisitions have forced the company to take on significant liabilities. The biggest three issues are:

1) Debt: ECL’s adjusted total debt, which includes over $400 million in off-balance sheet debt, stands at $7.6 billion (25% of market cap).

2) Underfunded Pensions: ECL’s 2011 merger with water treatment company Nalco added over 10,000 employees and more than doubled the company’s pension underfunding, which now stands at over $1.2 billion (4% of market cap).

{kind=link}

3) Employee Stock Options: The addition of new employees, as well as the appreciation of ECL stock this year, has brought ECL’s ESO liability up to $500 million (2% of market cap).

Combined, these liabilities add up to over $9.3 billion or 31% of the market cap. On their own, these liabilities aren’t enough to make ECL dangerous, but they do limit the amount the company will be able to spend in the future on acquisitions. ECL cannot keep buying up companies to fuel growth, at some point it will have to grow organically, which it hasn’t done well at in recent years.

The problem for equity holders is that ECL needs to keep growing rapidly to support is stock price. When analyzing the expectations embedded in its current valuation of ~$103/share, our DCF model shows that the market expects ECL to grow NOPAT by 15% compounded annually for 10 years. That’s an ambitious growth scenario for a company with declining ROIC and essentially flat margins.

{kind=link}

Both LF and ECL have seen significant bottom line growth in the past two years. However, the differences in the way the two companies achieved their growth and in their respective valuations make LF one our Most Attractive Stocks and ECL one of our Most Dangerous.

The Most Dangerous Stocks report for December can be purchased here, while the Most Attractive Stocks can be purchased here. To gain access to these reports one week earlier each month, e-mail us at[email protected] to request a subscription.

Sam McBride contributed to this report.

Disclosure: David Trainer owns AGO. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.