This report is one of a series on the adjustments we make to GAAP data so we can measure shareholder value accurately. This report focuses on an adjustment we make to our calculation ofeconomic book value and our discounted cash flow model.

We’ve already broken down the adjustments we make to NOPAT and invested capital. Many of the adjustments in this third and final section deal with how adjustments to those two metrics affect how we calculate the present value of future cash flows. Some adjustments represent senior claims to equity holders that reduce shareholder value while others are assets that we expect to be accretive to shareholder value.

Adjusting GAAP data to measure shareholder value should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

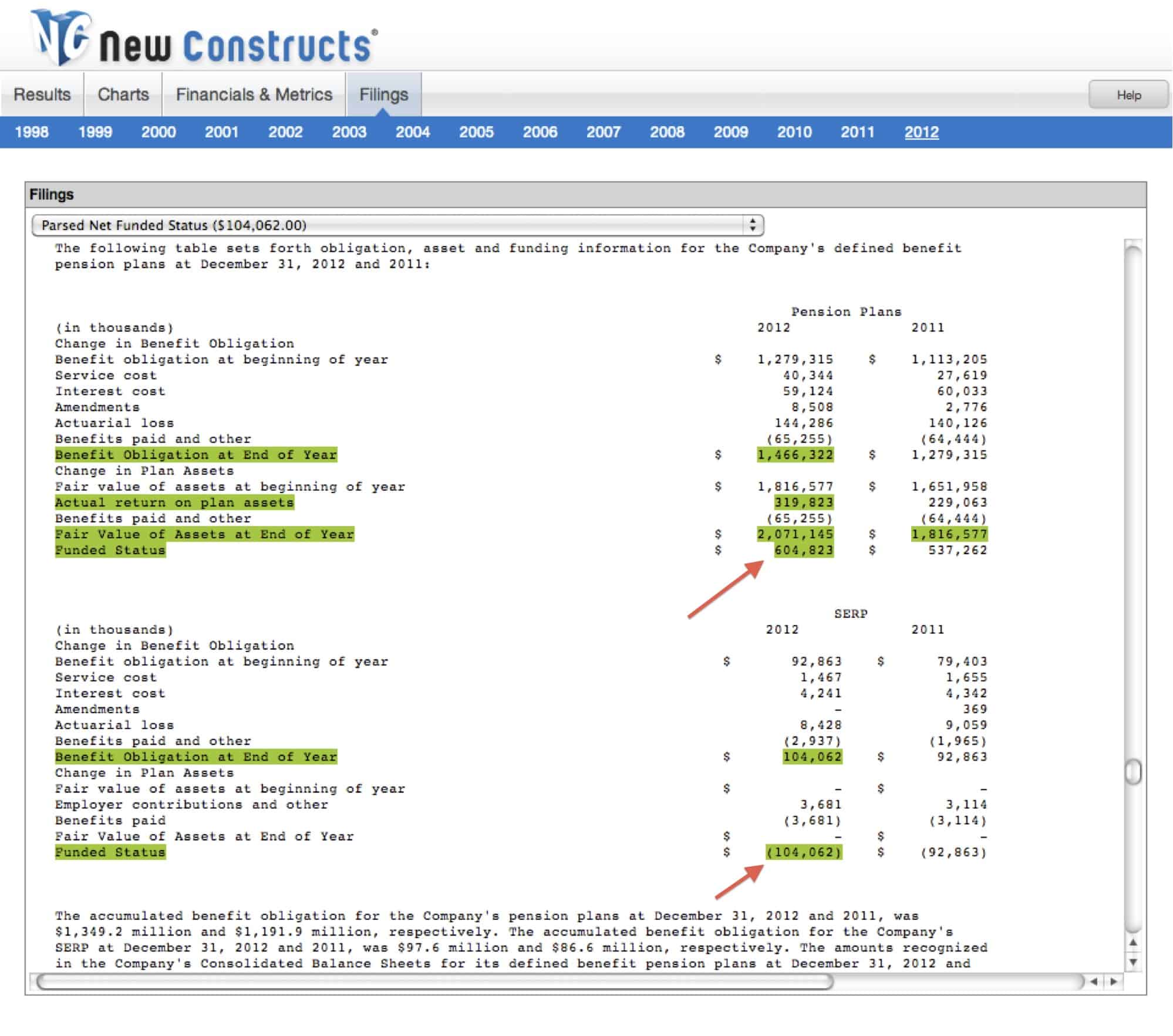

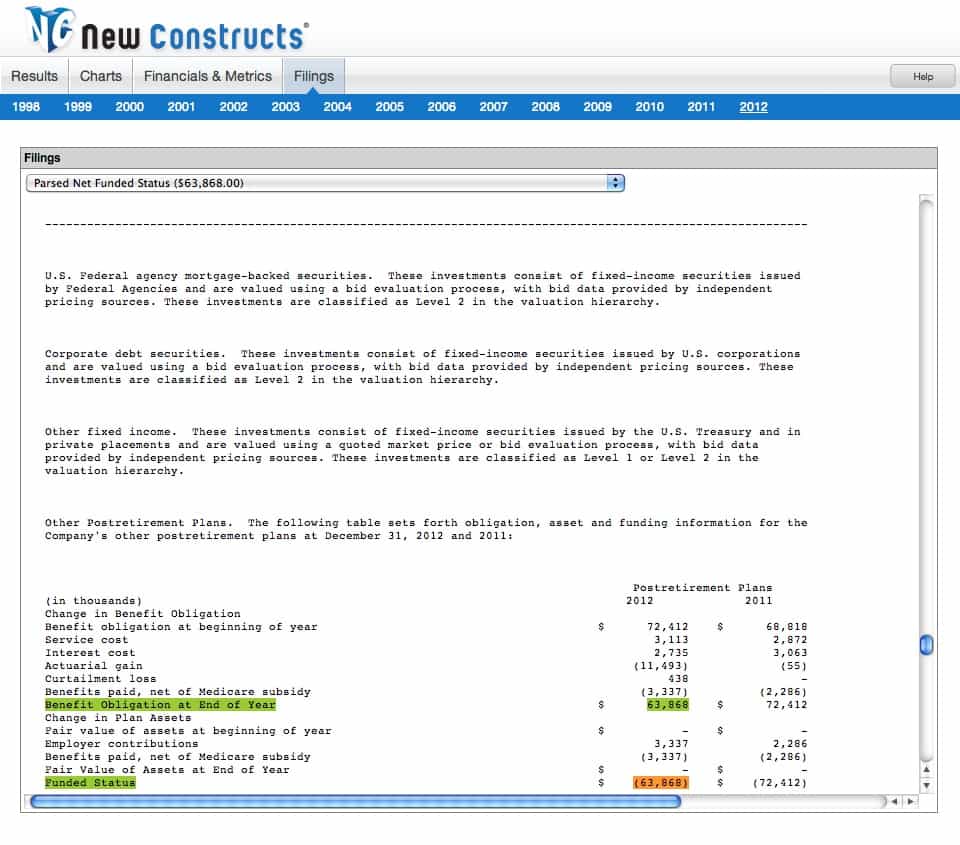

In their annual reports, companies disclose the value of the assets used to fund their pension plans and the present value of the future obligation, called the projected benefit obligation. The net funded status of a pension plan is the difference between these two values. A company with a positive net funded status has more assets than they need in their plan, which means future cash flows that would have been used to meet new obligations can instead be returned to shareholders. Companies with underfunded pensions will likely need to divert a greater amount of future cash flows away from shareholders to make up the funding gap. An accurate analysis of shareholder value should include the net funded status of pensions.

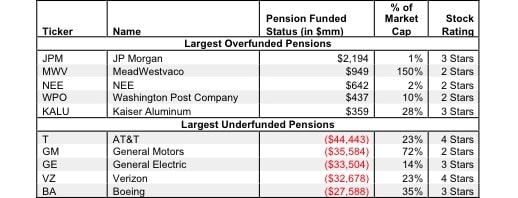

The Washington Post Company (WPO) is one of only a few publicly traded companies that have a net positive funded status for its pension plans. The company’s three pension and postretirement plans are currently overfunded by $437 million. Jeff Bezos may not be getting much in the way of profits from his acquisition of The Washington Post newspaper (which is one segment of the company), but at least he won’t be taking on any pension liabilities.

{kind=link}

{kind=link}

Without careful footnotes research, investors would never know that the pension net funded status can increase or decrease the amount of future cash flow available to shareholders.

Figure 1 shows the five companies with the largest overfunded pensions added to shareholder value in 2012 and the five companies with the largest underfunded pensions in 2012.

Figure 1: Companies With the Largest Pension Under/Over Funding Removed From/Added To Shareholder Value

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

The ten companies in Figure 1 are far from the only companies that are affected by the net funded status of pension plans. In 2012 alone, we found 45 companies with overfunded pensions totaling over $5.3 billion and 1,096 companies with underfunded pensions totaling over $811 billion. Companies clearly prefer to leave their pensions underfunded in order to boost short-term profits by committing cash elsewhere.

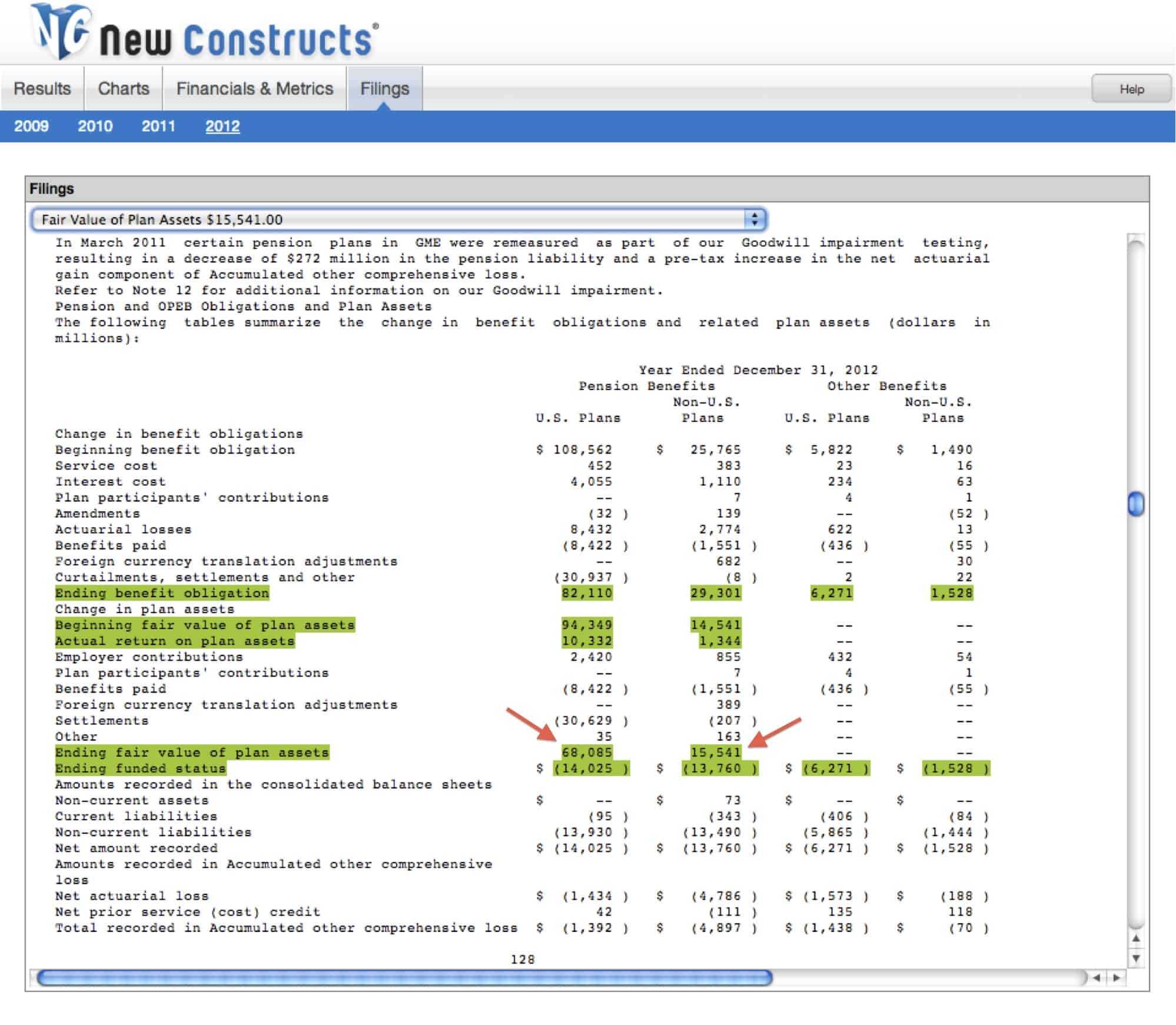

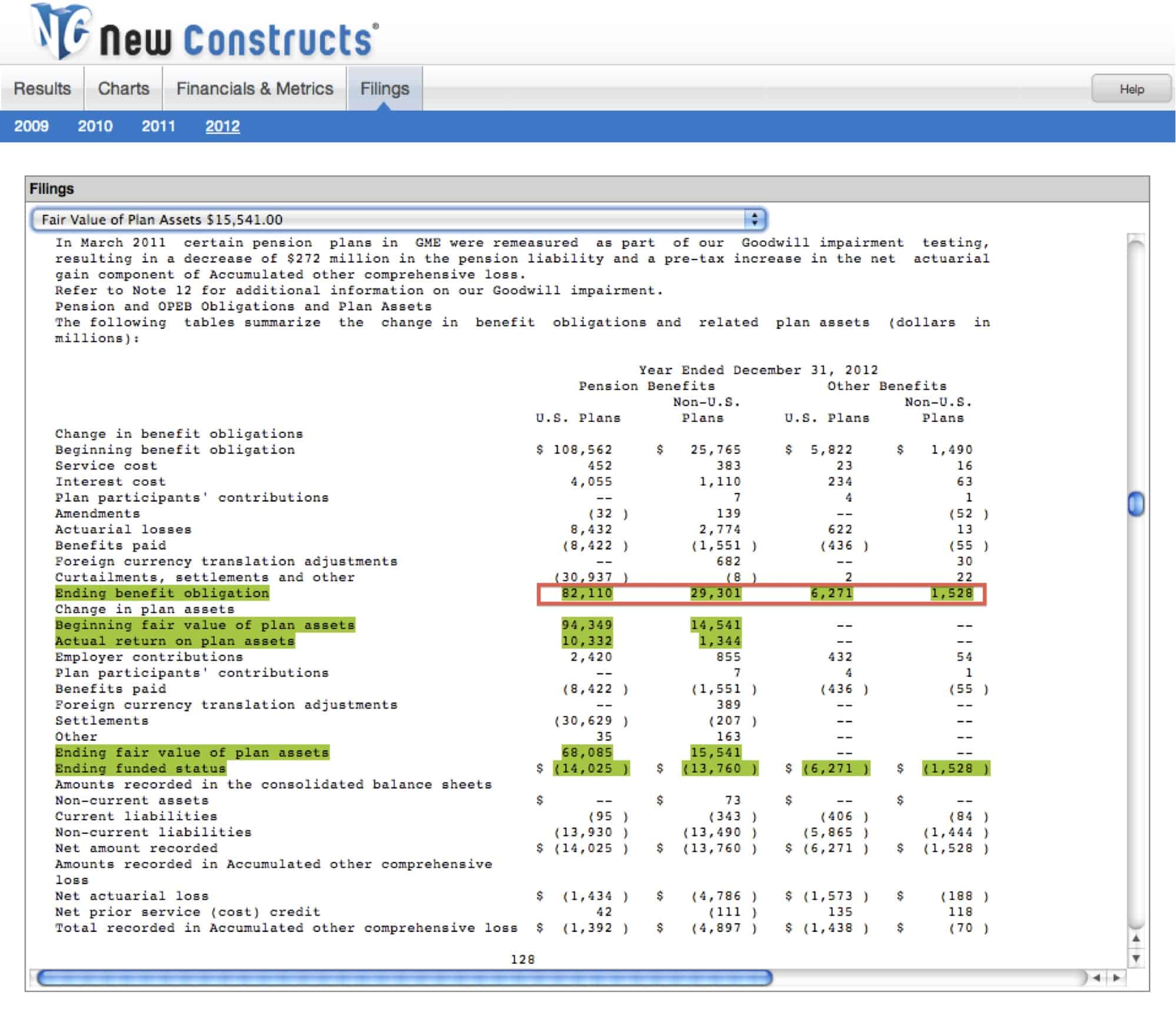

Since underfunded pensions decrease the amount of cash available to be returned to shareholders, companies with significant pension underfunding will have a meaningfully lowereconomic book value when this adjustment is applied. General Motors is one of the worst offenders for underfunded pensions. GM’s pension and postretirement plans have $84 billion in assets and $119 billion in projected benefit obligations.

{kind=link}

{kind=link}

Without removing the $35 billion in pension underfunding on GM’s books, the company would have a price to economic book value ratio of 1.1, which we classify as Very Attractive. Removing that $35 billion increases the ratio to 4.3, which qualifies as Very Dangerous.

Investors who ignore over and under funded pensions are not getting a true picture of the cash available to shareholders. Diligence pays.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.