With the midterm elections now just two months away and campaigning starting to heat up, we thought we would share our current views on the political landscape and what it may mean for U.S equities. In our two Outlook 2014 publications for this year, we posited that the U.S. economy and corporate profits may drive the stock market higher and investors could turn their attention away from policymakers in Washington, who were such a distraction in 2013 and earlier in the current economic expansion.

We continue to see opportunities for further stock market gains over the course of 2014, as discussed in our Mid-Year Outlook 2014: Investor’s Almanac Field Notes, based upon fundamentals rather than the potential for sweeping legislative change. Although our analysis of stock market performance around midterm elections is very supportive of our positive stock market outlook, it is not a key driver of that outlook.

This Election’s Impact May Be Smaller Than Usual

We do not expect politics to have a big impact on the stock market this fall for two reasons:

- There is not much uncertainty for the elections to remove. Markets hate the uncertainty that changes in Washington’s political landscape tend to bring. But there is no debt limit debate until March 2015 or spending cuts that need to be addressed over the near term as in recent years.

- Divided government will likely persist no matter the election outcome. Neither party is likely to gain a distinct advantage. We (and the consensus) fully expect that the election will leave us with a still divided government. Major policy initiatives such as tax reform or entitlement reform (as necessary as they may be) are unlikely to get done by the next Congress regardless of midterm election results.

It is highly likely that Republicans will maintain control of the House, where they currently hold a sizable majority that may widen. In the Senate, professional political forecasters and our contacts in Washington put the odds that Republicans regain control at between 60% and 70%.

The Senate Battle

To win the Senate, Republicans would need to win six of the 21 contested seats currently held by Democrats (assuming incumbent Republicans hold on to their 15 contested seats). If so divided government in Washington would persist for at least two more years, with a Democratic president and Republican Congress until the 2016 presidential election. Several of the contested seats currently being held by Democrats are in traditionally Republican-leaning (so-called red) states, which, along with fewer seats to defend, redistricting, and the latest polls, suggest Republican control of the House and Senate in 2015 – 2016 is more likely than not.

If the Republicans do not take control of the Senate, then a divided and gridlocked Congress returns. Although Washington is probably more likely to get some things done with Congress entirely under Republican control, especially as the Obama Administration moves more into legacy-building mode, major market-moving reforms are unlikely in either scenario.

This Doesn’t Mean Nothing Will Get Done

This outcome doesn’t mean policy is irrelevant and that nothing will get done in Washington over the next two years. A continuing resolution this fall will be needed to fund the government until after the 2014 elections. This may begin to turn the market’s attention to the next debt ceiling deadline in March 2015, which could have some political brinksmanship attached to it, although a default is very difficult to envision. We do not believe the Republicans have the appetite for another budget standoff that could result in another government shutdown or, worse, default. In addition, there appears to be bipartisan support for changes to energy policy that could come in 2015, regardless of the makeup of Congress. Infrastructure, immigration, and housing finance reform are also areas of potential compromise.

Stocks Embrace Midterm Elections

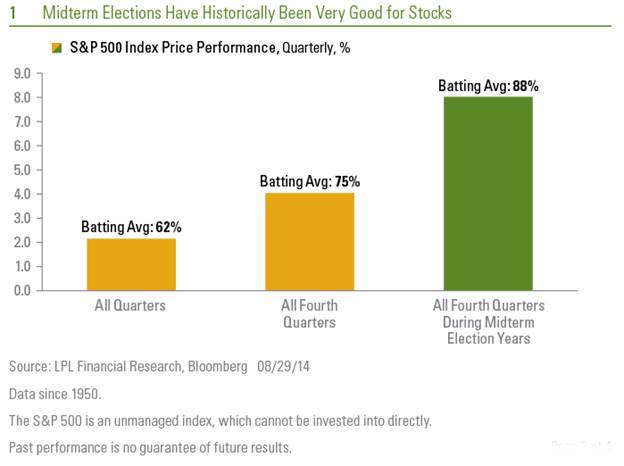

Though not a key piece of our positive outlook for the S&P 500, stocks seem to love midterm elections. Since World War II, the market’s reaction to midterm elections has almost always been positive, even when the balance of power has shifted in one or both houses of Congress — as would happen this year if the Republicans take the Senate. As shown in Figure 1, the fourth quarter in any year has been a good time to own stocks, but the fourth quarter during midterm election years — the quarter that begins on October 1, 2014 — has historically been a really good time to own stocks. In fact, 14 of the last 16 fourth quarters during midterm election years have seen the S&P 500 Index move higher, by an average of 8%.

A change in control has not changed this dynamic. In four of the five years that midterm elections resulted in a change in power (1954, when Democrats took the House; 1986, when Democrats took the Senate; 2002, when Republicans took the Senate; and 2006, when Democrats took the House and Senate), fourth quarter returns were positive, much like those in midterm election years when no change in power took place.

Interestingly, in the only two midterm election years since World War II during which U.S. equities did not experience a fourth quarter rally (1978 and 1994), the Federal Reserve (Fed) was aggressively hiking interest rates.

- In 1978, the lead-up to the Islamic Revolution resulted in strikes and unrest in Iran. In November 1978, a strike by Iranian oil workers reduced production from 6 million barrels per day to about 1.5 million barrels. At the same time, foreign oil workers fled the country. In the United States, inflation hit 9% in the fourth quarter of 1978 with no signs of slowing down as it approached double digits. In response to surging inflation, the Fed was aggressively hiking rates, with a total increase of 1.25% in the fourth quarter alone, pushing the policy rate up to 10%.

- In 1994, the S&P 500 turned in a roughly flat fourth quarter on the heels of a shift in power to the Republicans. However, the performance was less of a reaction to the election results than to rising fears of recession amid the Fed’s aggressive hiking of short-term interest rates and a corresponding run-up in long-term interest rates (to nearly 8% from below 6% at the start of the year). Although the Fed is currently withdrawing stimulus by phasing out quantitative easing (QE), we do not expect the Fed to raise interest rates until well into 2015. As a result, we do not expect the Fed to disrupt the stock market during the fourth quarter as it did during the fourth quarters of 1978 and 1994.

Bottom line, the resolution of election uncertainty—and ending the predominantly negative rhetoric surrounding the campaigns—has historically been a positive for the stock market and may help the S&P 500 reach new highs during the final stretch of 2014. And ending uncertainty seems to matter more to investors than the actual election results.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indices are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Stock investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Burt White is Managing Director and Chief Investment Officer at LPL Financial

Jeffrey Buchbinder is a Market Strategist at LPL Financial

{kind=link}