Is it possible for investors to buy cheap, profitable companies (have their cake) and still earn higher expected returns (eat it too)? Research indicates—yes, with some caveats.

In our book, Your Complete Guide to Factor-Based Investing, Andrew Berkin and I identified just five equity factors from the factor zoo that met all of the criteria we established for investing, a premium that was: persistent across time and economic regimes, pervasive across industries, countries, regions and asset classes; robust to various definitions; survives transactions costs; and has intuitive risk- or behavioral-based explanations for why the premium should be expected to persist. Two of the five were value and profitability (along with the related factor of quality, a broader measure than just profitability as it also includes low earnings volatility, low financial leverage, high asset turnover, low operating leverage and low idiosyncratic stock risk).

In our study, “Combining Value and Profitability Factors to Improve Performance,” published in the Journal of Beta Investment Strategies, Andrew Berkin and I showed that portfolios formed on the intersection of stocks with both high value and profitability characteristics outperformed portfolios with moderate characteristics, which in turn outperformed portfolios of stocks with low characteristics. These results were persistent, pervasive, robust, investable and intuitive, giving us greater faith in their continuing efficacy. We also showed that in contrast to the traditional value measure of book to market, value metrics using earnings and cash flow provide significant exposure to profitability and thus act as a useful complement. Our findings were consistent with those of Sunil Wahal and Eduardo Repetto, authors of the June 2020 study “On the Conjoint Nature of Value and Profitability” (summarized here).

Latest Research

Chris Satterthwaite and Lionel Smoler-Schatz of Verdad contribute to the factor investing literature in their research report “Combining Value and Quality,” in which they examine the relationship between value and quality in U.S. stocks. Their quality metric is gross profits/assets, taken from Robert Novy-Marx’s 2010 paper “The Other Side of Value: Good Growth and the Gross Profitability Premium.” Their data sample covers the period 1990-2024.

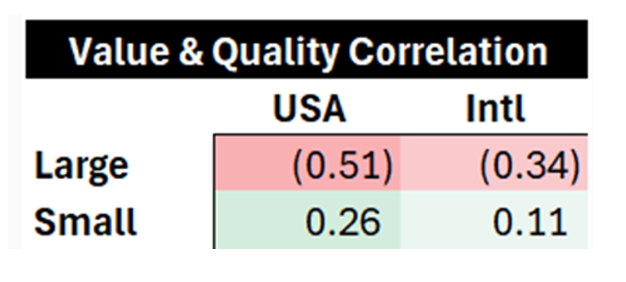

They began by asking: “Would you rather own a portfolio of cheap, low-quality companies or a portfolio of expensive, high-quality companies?” To answer that question, they scored the equity universe on their value factor (EV/sales, EV/EBITDA, P/E, P/B) and their quality factor (GP/assets). They then looked at the correlation between value and quality factor scores, separating the universe into large and small caps (defined as having a market cap < $1 billion) for both the U.S. and international equities. At least in large stocks, their findings were as you might logically expect: there was a negative correlation between quality and value—on average, higher quality (more profitable) companies were more expensive. However, this was not true in small caps, where the relationship was positive—higher quality (more profitable) companies were actually cheaper—a behavioral anomaly (explained by retail investor preference for lottery-like stocks).

To test the robustness of their findings, Satterthwaite and Smoler-Schatz also examined quality as measured by a blend of ROE, ROA, ROIC and EBITDA margin and saw the same trends emerge.

They then examined how buying small, cheap and profitable companies has improved returns.

As you can see in the above tables, more profitable firms delivered higher returns in both small and large stocks. However, the returns to high profitability cheap companies were much greater in small stocks (12.6% versus 9.6% in large stocks on a market-cap weighting basis and 21.0% versus 8.6% on an equal-weighted basis). The reason is that the expensive, high profitability, large stocks had virtually the same return as the cheap, high profitability, large stocks, while the cheap, high profitability, small stocks had much higher returns than the expensive, high profitability, small stocks.

Combining factors not only works with value and profitability. In their 2013 study “A New Core Equity Paradigm,” Andrea Frazzini, Tobias Moskowitz and Robert Novy-Marx showed that combining value, profitability and momentum not only produced more efficient, diversified, long-only portfolios but also that these factors go a long way toward explaining why some portfolio managers excel—they have greater exposure to these factors using efficient construction rules to minimize the negative impact of trading costs.

Further Support for Multi-Factor Portfolios

In his April 2022 paper, “Combining Factors,” Christoph Reschenhofer investigated the performance of multifactor portfolios and found that factor premiums were all greater in small stocks than in large stocks and that when comparing single characteristic portfolios with multivariate characteristic portfolios (where the aggregate score was calculated as the equally weighted average of the individual scores), averaging multiple firm characteristic scores produced portfolios with more favorable risk-return characteristics (lower volatility and higher after-cost returns) than the market and those of portfolios sorted on univariate characteristics. The small-cap (large-cap) portfolio exhibited a 70 percent (25 percent) increase in Sharpe ratio after transaction cost compared to the market portfolio.

Investor Takeaways

The empirical evidence we reviewed provides support for multiple characteristics-based scorings to form long-only factor portfolios, encouraging the combination of slow-moving characteristics (such as value, investment and/or profitability) conditional on fast-moving characteristics (such as momentum) to reduce portfolio turnover and transactions cost. Fund families, such as AQR, Avantis, Bridgeway and Dimensional, use such an approach, integrating multiple characteristics into their portfolios conditionally on momentum signals. The research also demonstrates the important role that portfolio construction rules (such as creating efficient buy and hold ranges or imposing screens that exclude stocks with negative momentum) play in determining not only the risk and expected return of a portfolio but also how efficiently the strategy can be implemented (considering the impact of turnover and trading costs)—wide (narrow) thresholds reduce (increase) portfolio turnover and transactions costs, thereby increasing after-cost returns and Sharpe ratios. (Note that there is a tradeoff in that wider bands lower the exposure to the desired characteristics—so returns could decrease both before and after costs if the bands are too wide.)

Larry Swedroe is the author or co-author of 18 books on investing, including his latest, Enrich Your Future: The Keys to Successful Investing.