A while ago -- admittedly a long time ago -- hedge fund customers had all the fun. Investors obtained their non-correlated giggles through diverse strategies such as trading around mergers, following futures markets trends, pitting long equity positions against shorts and, among others, fixed income arbitrage.

Though there hasn’t been much joy in Hedgeville over the past couple of years, some wan smiles could be seen the faces of investors in 2012. Halfway through the year, fixed income arbitrage was the best performer among the dozen strategies subsumed within the Dow Jones Credit Suisse Hedge Fund Index. With interest rates so low nowadays, it’s no wonder that yield-hungry investors would be especially keen on plays designed to squeeze a little extra out of the bond market.

In their quest for alpha, hedge fund managers employ a number of market-neutral arbitrage tactics to exploit valuation differences between fixed income securities or contracts.

Fixed Income Tactics

- Swap Spread Arbitrage

In a typical trade, an arbitrageur starts with a swap in which a floating rate is paid in exchange for the receipt of a fixed coupon rate. A second leg consists of a short Treasury bond position matching the maturity of the swap. The bond sale proceeds are then invested through a margin account at the “repo” or repurchase agreement rate.. Essentially, the trade is a bet that the fixed rate remains higher than the floating rate over the swap’s life. (When floating rates are expected to rise, the trades and resulting cash flows are reversed).

- Volatility Arbitrage

Most commonly, volatility arbitrage entails the sale of options against a fixed income inventory position. As long as market-neutrality is maintained (i.e., the delta of the bond and option positions offset), the excess volatility embedded in the option premium can be harvested as profit.

- Capital Structure Arbitrage

Capital structure arbitrage exploits mispricings in an issuer’s securities or changes in market demand for the paper. An arb may, for example, purchase a company’s senior bonds and sell short its subordinated debt, hoping a bull market narrows the yield spread.

- Mortgage Arbitrage

Hedging mortgage-backed securities with swaps is a common arbitrage. A duration-weighted hedge isolates the pre-payment risk embedded in a mortgage pool.

- Yield Curve Arbitrage

Taking long and short positions at different points along the yield curve allows a trader to exploit the relative cheapness/richness of certain maturity buckets or to capture gains from the wholesale flattening/steeping in the slope.

Among fixed income arbitrage trades, those focused on the yield curve have drawn the most investor attention recently. The Treasury curve, in particular, has taken center stage since the Federal Reserve announced a swap of its short-term paper inventory for longer-dated obligations under the quaint moniker of “Operation Twist.”

Operation Twist is designed to nudge down long T-note rates. Since many loans are keyed off these securities, the Fed thinks this should stimulate spending and borrowing. Mechanically, the swap flattens the yield curve as the central bank sells Treasury securities maturing in less than three years and reinvests the proceeds in notes and bonds maturing six to 30 years out.

So far, it’s worked well. At least the curve has flattened (it’s debatable whether the operation’s actually encouraged people to part with their cash or to take on debt). From September 21, 2011, when the program was announced, through mid-2012, a fifth of the spread between two-year and ten-year T-notes has been trimmed.

Now you’d think that would be good news for the hedgies. After all, the Fed blatantly telegraphed its intent long before tweaking its inventory. Traders could have easily piggybacked on the central bank’s open market operation and surfed toward the long end of the yield curve.

Surprisingly, though, the Dow Jones Credit Suisse Fixed Income Arbitrage Hedge Fund Index has been pretty much flat since the Twist party started. The reason? Well, the benchmark’s performance reflects the constituent funds’ emphasis on other arbitrage styles, i.e, their de-emphasis of the Treasury market. No single product in the index focuses solely on riding the Treasury yield curve waves.

In fact, the pure-play opportunities are available through exchange-traded products. There are a number of funds and notes that investors can use either as surrogates for vanilla Treasury portfolios or as proxies for “twist” operations. Keeping in mind that past performance is never a guarantee of future results, we may be able to glean some insight into the relative sensitivity of these products to future Fed action with a bit of a look-back.

Yield Curve Dynamics

By now, it shouldn’t be a surprise that investors scoop up Treasury paper whenever the global or domestic economy hiccups. The impact of these “risk off” trades is predictable. In the first nine months of 2011 leading up to the Fed’s announcement of Operation Twist, the market yield on the ten-year T-note fell more than 30 basis points. Back then, though, investors were more keenly interested in shorter maturities. Yields on two-year paper dropped by 40 basis points. All this steepened the Treasury yield curve.

That all changed with Operation Twist. By mid-2012, ten-year yields were halved while those of two-year paper actually ticked up. All told, the curve between these maturities flattened by more than 150 basis points in the nine months following the Fed’s intervention.

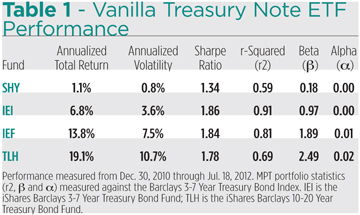

So what effect did this have on investors? As you might expect, holders of longer-dated T-notes or their exchange-traded fund analogs benefited most. The iShares Barclays 7-10 Year Treasury Bond Fund (NYSE: IEF) rose at a 13.8 percent rate since the beginning of 2011 while its sibling iShares 1-3 Year Treasury Bond Fund (NYSE: SHY) appreciated by just 1.1 percent (see Table 1).

From the table, you’ll readily see the direct relationship between fund returns and volatility. Here, risk -- at least that associated with stretching out on the investment horizon -- seems amply rewarded. The IEF fund’s higher Sharpe ratio and positive alpha, compared to SHY, obliquely reflect the yield compression in the Treasury market over the past 18 months.

Other exchange-traded products more directly trace changes in the shape of Treasury curve. There’s a pair of Barclays Bank notes, for example, that track the Barclays Capital US Treasury 2Y/10Y Yield Curve Index. The index simulates a spread between two-year and ten-year T-note futures.

Holders of the iPath US Treasury Steepener ETN (NYSE Arca: STPP) make money when the spread in Treasury yields widens (i.e., the curve steepens) while its opposite, the iPath US Treasury Flattener (NYSE Arca: FLAT) gains when the spread narrows.

The ETNs’ underlying index captures these returns through a notional rolling investment in T-note futures contracts, weighted 75% in the two-year maturity and 25% in the ten-year. The index’s weighted average maturity is four years, making the spread directly comparable, for benchmarking purposes, to the Barclays 3-7 Year Treasury Index we’ve used to gauge the performance of the long-only Treasury funds.

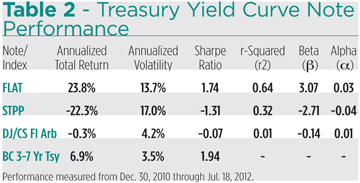

It should come as no surprise that the implementation of Operation Twist has been a boon for FLAT investors and a detriment to holders of the STPP note. Table 2 depicts the portfolio statistics of both iPath products together with the Dow Jones Credit Suisse Fixed Income Arbitrage Hedge Fund Index. Here, we’ve benchmarked the notes and the hedge fund index to the Barclays standard over the same investment horizon used in our previous analysis.

What’s noteworthy (an unintended pun), though not really surprising, is FLAT’s positive alpha. The note’s 24 percent return -- better than three times that of the benchmark -- readily swamped its high beta. With that in mind, you well might ask how the hedge fund index’s negative return still entitles it to positive alpha. That’s also explained by beta. Keep in mind that alpha quantifies a security’s beta-adjusted excess return over the benchmark The hedgies paradoxically delivered on their promise of non-correlated returns by keeping their r-squared coefficients low and their betas negative. Unfortunately, investors can’t eat negative beta.

FLAT’s return can’t be attributed solely to a change in the contour of the yield curve, though. A curve of another sort contributes excess return (either positive or negative). Remember FLAT’s underlying index tracks a weighted futures spread. The underlying Barclays index is nominally long 75 percent two-year note contracts and 25 percent short ten-year futures, but FLAT delivers the inverse index return, comparable (though not necessarily equivalent) to holding positions opposite the benchmark.

It’s important to recall that holders of futures open interest must roll their positions from one delivery month to the next as their contracts approach expiration. This is done to avoid conveyance of the underlying Treasury notes. For FLAT that means two swaps are negotiated each calendar quarter: a rough approximation of rolling forward a long ten-year note position and a short stance in two-year futures.

More often than not, deferred deliveries of interest rate futures are priced at a discount to nearbys, reflecting the time value of money. In such a backward environment (compared to the contango found in adequately supplied markets for storable commodities), quarterly rolls of long positions engender incremental gains while the extension of short postures yields losses. With rolls, it’s nothing more than “selling high and buying low.” The weighting scheme of the index produces overshadowing gains at each swap, but FLAT investors see a negative roll yield (remember, the ETN delivers an inverse return) as long as the T-note futures market remains backwardated.

There’s a couple of lessons here. First, a backwardated T-note futures market favors STPP investors. Second -- really a corollary of the first -- is that a tip into a contango market turns things upside down. That’s likely if the yield curve inverts (short rates exceed long rates).

The Future

To manage economic recoveries, the Federal Reserve typically ratchets up short-term rates, flattening out the Treasury yield curve. The current environment has hardly been typical, however. After supplying liquidity for such a long time on the heels of the 2008-2009 crash, there wasn’t a lot of maneuvering room left at the short end, so last year central bankers dug into their playbook to reprise a 1961 strategy and extended the Fed’s direct influence on maturities further out.

All that’s going to end some day. Sooner or later, the yield curve will reach a sort of stasis, featuring parallel changes on either end, or will actually steepen. At that point, the utility and the outperformance of the FLAT ETN will likely be foreclosed. At some date we may see STPP become the darling of Fed watchers. We don’t yet know if the central bank will signal a course reversal as well as it telegraphed the onset of Operation Twist. Suffice for now to know that there are products that can tactically exploit or hedge against this policy shift.

Fun, right?