Properly-structured life insurance is an asset that can add value to any portfolio, yet many financial advisors have traditionally shied away from offering life insurance policies to their clients. That’s because life insurance is often viewed as difficult to sell, hard to understand, and, frankly, not worth the effort. Indeed, a recent survey found that advisors didn’t offer life insurance products to their clients because they perceive it to be complex and lacking liquidity.1 But not all life insurance is created equal. While many advisors’ objections to selling life insurance are founded in fact, an evolution in the insurance market has led to new products that help address many of their concerns.

Solving the insurance conundrum

Research shows that to meet changing needs, clients are twice as likely to surrender or exchange their policy as they are to have the death benefit paid out.2 “Often, clients see high surrender penalties that hinder their ability to get money out of the contract if they have a hardship,” says Gene Lunman, executive vice president of MetLife Retail Life & Disability Insurance. “So that’s one reason why we created MetLife Premier Accumulator Universal Life, which can provide clients with both liquidity and flexibility.”

MetLife’s Premier Accumulator Universal Life (PAUL) provides higher early cash value accumulation than traditional life insurance policies, as well as surrender charges that are just 1% of charges built into typical whole life policies. These features mean that clients have the potential to access most or all of what they put into the policy within the first few policy years3, providing them with liquidity and the option to exit the policy if their needs change.

Rethinking compensation

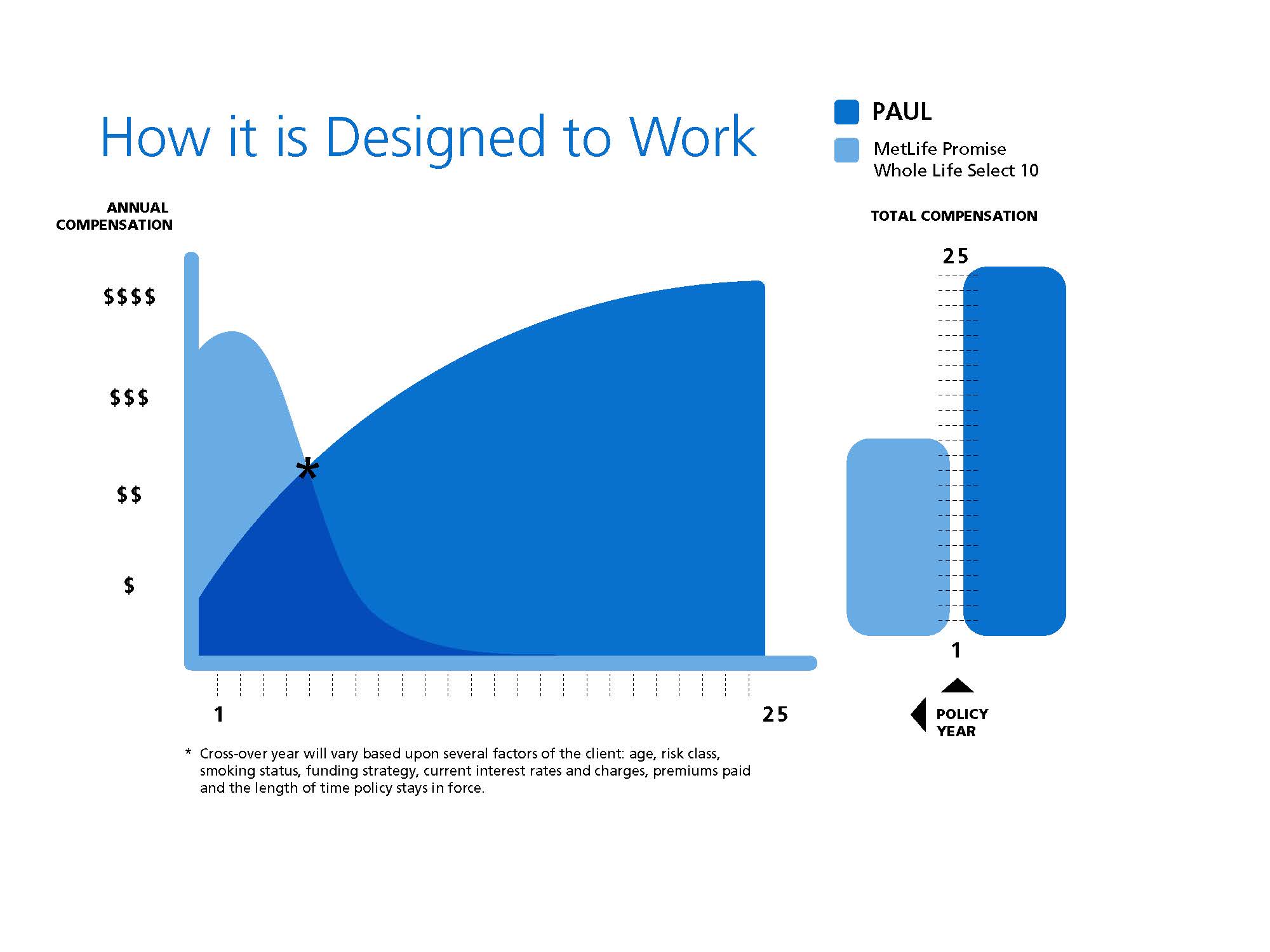

Compensation structures bear some of the blame for the high surrender costs of traditional life insurance. For many years, agents who sold life insurance received upfront, or “heaped,” compensation.

Rethinking that traditional compensation model allows for a whole new approach. By basing compensation on the policy’s cash value and premiums paid, and providing an asset trail rather than “heaped” compensation, PAUL is able to provide low surrender charges while also potentially providing a larger payment to the advisor over the life of the policy than a traditional whole life policy.

Simplifying the process

The process of purchasing life insurance has traditionally been taxing for clients, who typically must undergo rigorous medical exams. Fortunately, underwriting can be simpler and easier for eligible clients with PAUL, thanks to MetLife Enhanced Rate PlusSM (ERP). Qualified applicants go through a 20-40 minute telephone interview; paramedical exams or lab work may not be necessary4. That means that the underwriting process can be reduced from a month or more to just one week. This streamlined process also more closely matches the way advisors are compensated for selling other financial assets. PAUL with Enhanced Rate Plus allows clients the opportunity to get a policy faster—and financial professionals to get paid faster.

Meeting wide-ranging needs

With PAUL, MetLife is furthering its commitment to creating products designed to meet the wide-ranging needs of its diverse clients and advisors. “The good news with PAUL is that the consumer gets the death benefit protection they want or the living benefit they need in the form of higher cash value3; the advisor gets a more familiar compensation structure, and the streamlined ERP underwriting process makes the entire process go very quickly for qualified clients,” says Lunman. In short, both advisors and their clients benefit.

For more information, watch this video.

Any discussion of taxes is for general informational purposes only, does not purport to be complete or cover every situation, and should not be construed as legal, tax or accounting advice. Clients should confer with their qualified legal, tax and accounting advisors as appropriate.

MetLife Premier Accumulator Universal Life is issued by MetLife Insurance Company USA on Policy Form 5E-37-14 and in New York only by Metropolitan Life Insurance Company on Policy Form 1E-37-14-NY. All product guarantees are subject to the financial strength and claims-paying ability of the issuing insurance company. L0715430444[exp0716][All States]

[1] WealthManagement.com, “2015 Investment Trend Monitor Survey: Advisor Views On Variable Annuities,” 2015.

[2] MetLife Internal Study of the Statutory Annual Statements of 10 Large Life Insurance Carriers

[3] Based on current interest rates and charges which are not guaranteed. Cash value is accessed through withdrawals and loans which will reduce the policy's cash value and death benefit.

[4] All eligible clients who qualify for Standard Rates without an extra premium will receive the upgrade. Clients with certain factors - including, but not limited to, ratable medical impairments and other health or lifestyle risks that require an extra premium - do not qualify for Standard Rates or program upgrades and will proceed through traditional underwriting.

{kind=link}