By Todd Eckler

The 2017 Tax Cuts and Jobs Act has been something of a mixed bag for high-net-worth families. The 260-basis-point cut of the top individual tax rate and the increased threshold to enter the highest tax bracket for married couples filing jointly were two of the benefits that came out of the December legislation. However, the new law also contains some challenges for high-income earners—notably, the new $10,000 cap on deductions of state and local income and real estate taxes. If there is a silver lining, however, it is that more high-net-worth households could be able to utilize charitable gift “bunching” to increase their total deductions over a few years.

While the technique may have been used more sparingly under earlier tax regimes, under the new law, charitable gift bunching may prove to be beneficial to donors whose non-charitable itemized deductions fall below the new higher standard deduction ($24,000 for married persons filing jointly).

“Bunching” involves consolidating tax-deductible charitable contributions that would normally be made over multiple years into a single tax year. In the consolidated year, the donor contributes to a charitable giving vehicle, such as a donor-advised fund with a sponsoring nonprofit and receives an immediate tax deduction through itemizing deductions on their federal tax return. The donor would then recommend grants from the DAF to qualified charities over several years. While the higher standard deduction would still apply in certain years, the donor would benefit from being able to itemize deductions in the year of the contribution, which could improve total tax efficiency over time.

A Case Study on Gift Bunching

In the right circumstances, bunching strategies can make a notable difference. Consider, for instance, the following scenario involving a married couple filing jointly, outlined below. The hypothetical example underscores how bunching tactics can be applied as well as the considerable longer-term impact these techniques can have on tax deductions.

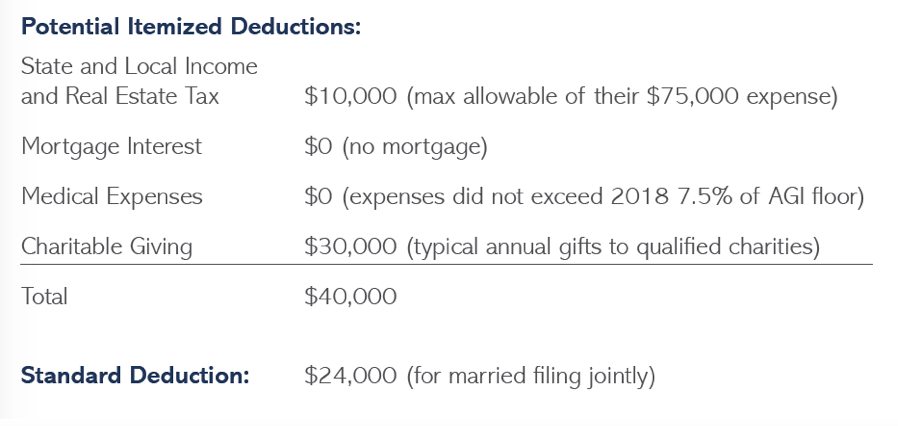

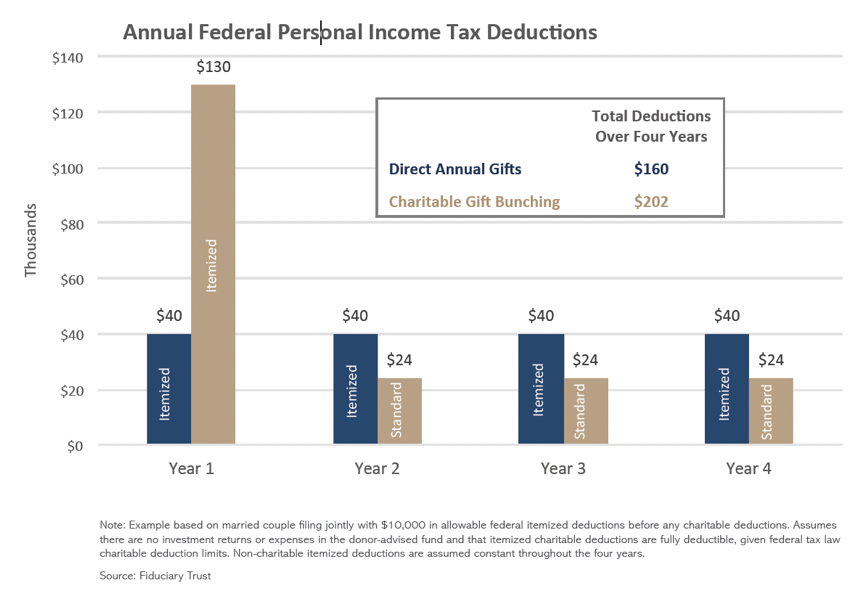

For instance, using a more traditional gifting approach in which donations are made directly to charitable organizations on an annual basis, the couple would lower their federal tax bill by itemizing their $40,000 in deductions rather than electing the $24,000 standard deduction. Assuming their deductions did not change, over a 4-year period the couple would benefit from a cumulative $160,000 in federal tax deductions.

Using the charitable gift bunching approach, however, can offer more flexibility and a higher overall level of deductions. Again, using the same assumptions outlined above, the couple would fund a DAF in the first year with $120,000 in appreciated securities—an amount equaling 4 years of their planned charitable giving. Since their federal adjusted gross income is greater than $400,000, they can fully deduct the DAF contribution, as it’s less than 30 percent of their AGI. (The deduction limit of 60 percent of AGI applies for charitable cash contributions, while unused deductions can generally be carried forward for up to 5 years into the future.) Combining the charitable contribution with their $10,000 of deductible state income and real estate taxes, the couple could take a $130,000 itemized deduction in Year One for federal tax purposes. Although the couple could also donate cash to the DAF in this bunching approach, donating appreciated securities held for more than 1 year also eliminates the capital gains tax associated with the securities’ appreciation.

Since their only potential itemized deduction in years 2 through 4 would be the $10,000 in state and local income and real estate taxes, the couple could then elect to take the higher $24,000 standard deduction in each of the 3 years. Across the 4 years covered by their bunched donation, they would receive $202,000 in federal tax deductions. During each of those 4 years, the couple could recommend that $30,000 in grants be made from the DAF annually to the IRS-qualified charities they select, or they could recommend differing grant sizes based on the organization’s specific needs in a given year. This speaks to the flexibility offered through DAFs.

The takeaway, though, is that through charitable gift bunching the couple would generate total tax deductions of $202,000 over the 4 years, compared to the $160,000 generated without bunching. The additional $42,000 in tax deductions would likely result in lower taxes, assuming that the couple’s AGI and federal tax rates remained constant throughout the 4-year period.

Before implementing a charitable gift bunching approach, however, it is important to examine the factors specific to each family’s financial situation, the charitable giving vehicles used and their charitable objectives. In all cases, families should consult with their tax and wealth advisors to see if charitable gift bunching is the best practice, and if appropriate, to determine how best to implement this technique.

Todd H. Eckler is the Executive Director of Fiduciary Trust Charitable, an independent public charity offering donor-advised funds and related services to clients and independent investment advisors who manage assets on behalf of donors.