By Brian Chappatta

(Bloomberg Opinion) --Jeffrey Gundlach is worried that investors are getting suckered into buying the dip in stocks, high-yield bonds and leveraged loans.

In his annual “Just Markets” webcast on Tuesday, DoubleLine Capital’s chief investment officer sounded off on a range of topics, including Bitcoin, Federal Reserve Chairman Jerome Powell’s “pivot,” the growth of the U.S. national debt, and the problem of underfunded state and local government pension plans. But it was the “BTFD” (Buy the Failed Dip) mentality that’s lasted for so long in risky corners of the financial market that had him drawing comparisons to the subprime mortgage crisis. He explained his chief cause for concern:

“People were panicking in the later part of December. They were panicking, actually, but the flow data shows they were panicking into stocks, not out of stocks. People have been so programmed, and feel so frustrated by selling when we get dips, that this time they weren’t going to be fooled. This time, they were going to buy the dip. I worry about that, though, because it reminds me a little bit about how the credit crisis developed in 2007 and 2008.”

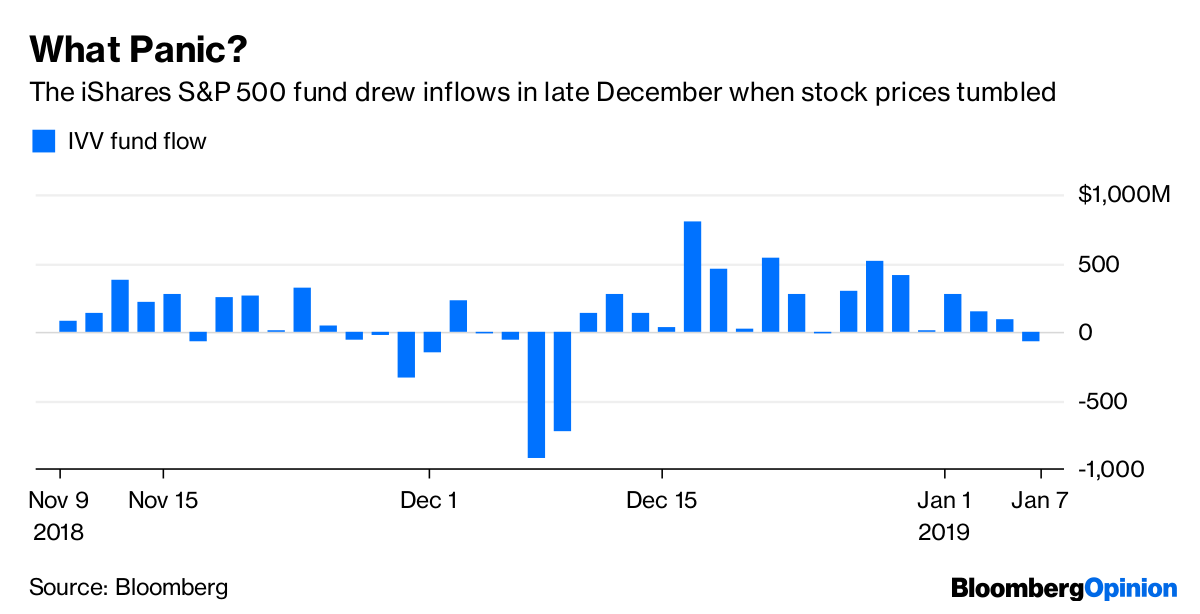

He’s right. A quick look at fund flow data for the iShares Core S&P 500 exchange-traded fund (IVV) and the SPDR S&P 500 ETF (SPY) tells the story. The iShares fund avoided outflows from Dec. 11 through the end of last week, even as stocks fluctuated wildly, data compiled by Bloomberg show. The SPDR fund drew the most money since February on Dec. 21, the day it tumbled 2.62 percent, part of the fund’s longest losing streak since January 2008.

Whoever did that is “feeling good today,” Gundlach said. But he offered a reminder of what happened to investors more than a decade ago who snapped up subprime mortgages at what they thought were low prices.

“The people who bought the dip, they didn’t sell, they hung on, and the market started to crack again. And we have that waterfall that ended up happening. The people who bought the dip ended up getting scared and turned from buyers into sellers. There’s potential for that here.”

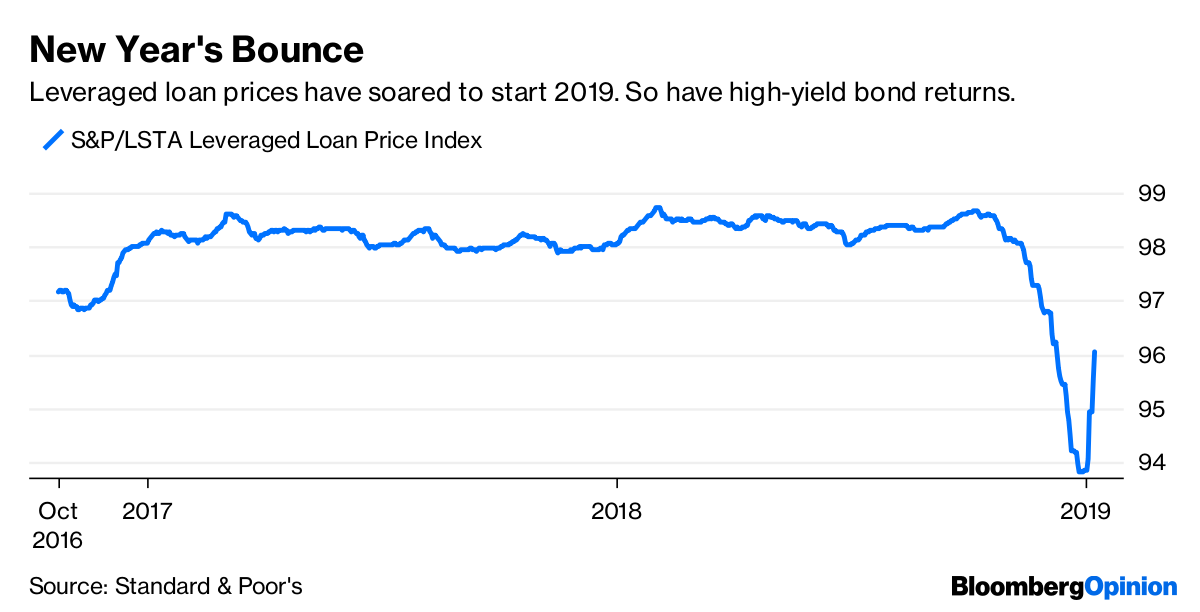

It’s not just the U.S. stock market that’s witnessing this, either. Junk bonds have come roaring back, with the Bloomberg Barclays U.S. Corporate High Yield Bond Index already returning 2.5 percent so far in 2019. The average price of leveraged loans, as measured by the S&P/LSTA Leveraged Loan Index, is up to 96 cents, compared with 93.8 cents at the end of 2018. Investors should use this recent strength in junk bonds “as a gift, and get out of them,” Gundlach said.

“Investors bought bank loans and high yield, I can understand why you buy the dip, I get it, buying the dip certainly worked back in 2016 and if you missed that, you feel bad about it. But like I said about subprime back in 2007, the first people, they buy the dip, they’ve never done that before, but they’ve been trained now to do it after continued frustration for not doing so, and then when prices head lower, suddenly those buyers turn into sellers, and with all the supply that’s coming, it’s a really interesting issue who’s going to buy it.”

All of this is to say Gundlach doesn’t seem to be a fan of risky investments at these prices. By his thinking, capital preservation is key because markets may be approaching the point at which some of these dips are going to end up being much more than just that. Though he wouldn’t necessarily load up on long-term U.S. Treasuries, either — that rally might be over, after a nice rebound to end 2018, he said.

Dismiss his gloomy outlook if you wish, but, as Bloomberg News’s John Gittelsohn noted ahead of the webcast, a lot of what Gundlach predicted in 2018 came true. He called for U.S. equities to rise early in 2018 but then eventually reverse and leave the market down for the year. He nailed the direction of stocks better than some of his equity counterparts.

If you’re an active fund manager, it’s hard not to sympathize with his view on buying the dip. It has been so prevalent, for so long, that it seemed almost inevitable that the late 2018 drop wouldn’t last. The wave of cash coming into passive ETFs tracking the S&P 500, even as the market tumbled, says it all.

No one is perfect when it comes to predictions, but Gundlach’s 2018 calls were largely spot on. If that happens again in 2019, investors had better buckle up for some turbulent times.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

To contact the author of this story: Brian Chappatta at [email protected]

For more columns from Bloomberg View, visit bloomberg.com/view