Our Most Attractive and Most Dangerous stocks for October were made available to the public at midnight on Wednesday. Last month saw some strong performances from our picks. MTR Gaming Group (MNTG) led the way for our Most Attractive stocks by gaining 24% in September. Lancaster Colony Corp. (LANC) was our top performing Large/Mid cap with a 9% gain. On the Dangerous side, recent Danger Zone pickInnerWorkings (INWK) dropped 11% in September while Electronic Arts (EA) declined by 9%.

October sees 13 new stocks make our Most Attractive list and 16 new stocks fall into the Most Dangerous category. Our Most Attractive stocks have high and rising return on invested capital (ROIC) and low price to economic book value ratios. Most Dangerous stocks have misleading earnings and long growth appreciation periods implied in their market valuations.

Most Attractive Stock Feature for October: DNB

The Dun & Bradstreet Corp (DNB) is one of the new additions to the Most Attractive list this month. DNB made the list due to the decrease in the attractiveness of other stocks on the list.

DNB has a top-quintile ROIC of 22%. It has also grown after-tax profit (NOPAT) by 8% compounded annually over the past decade.

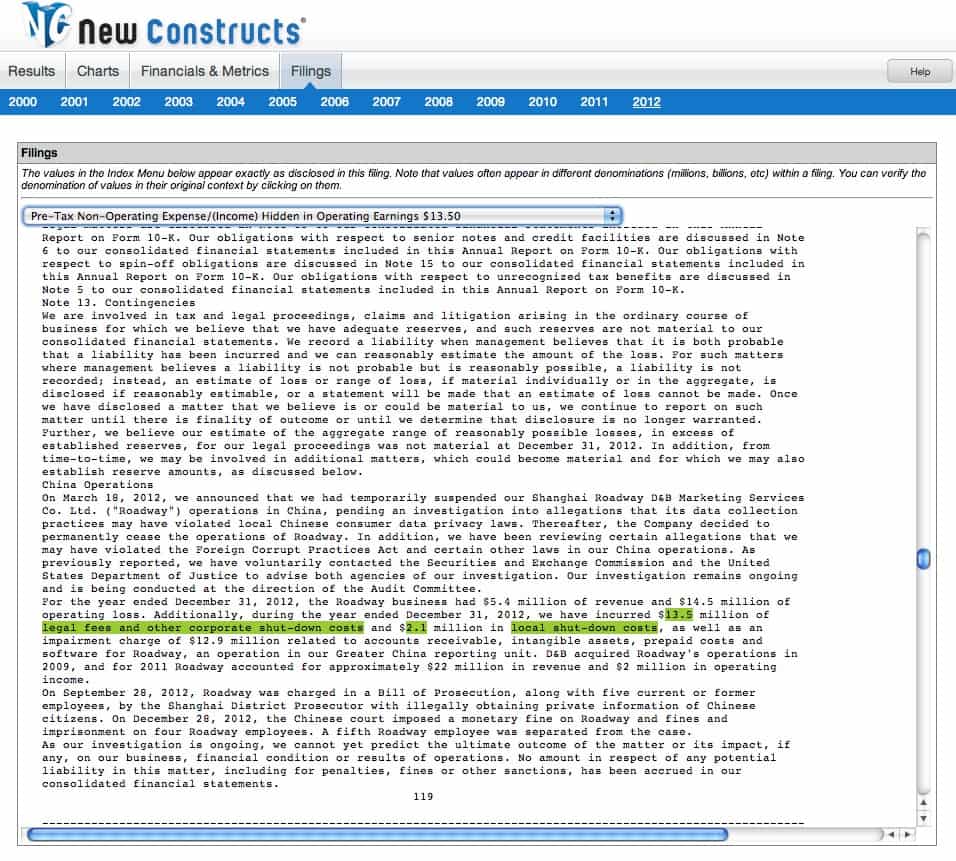

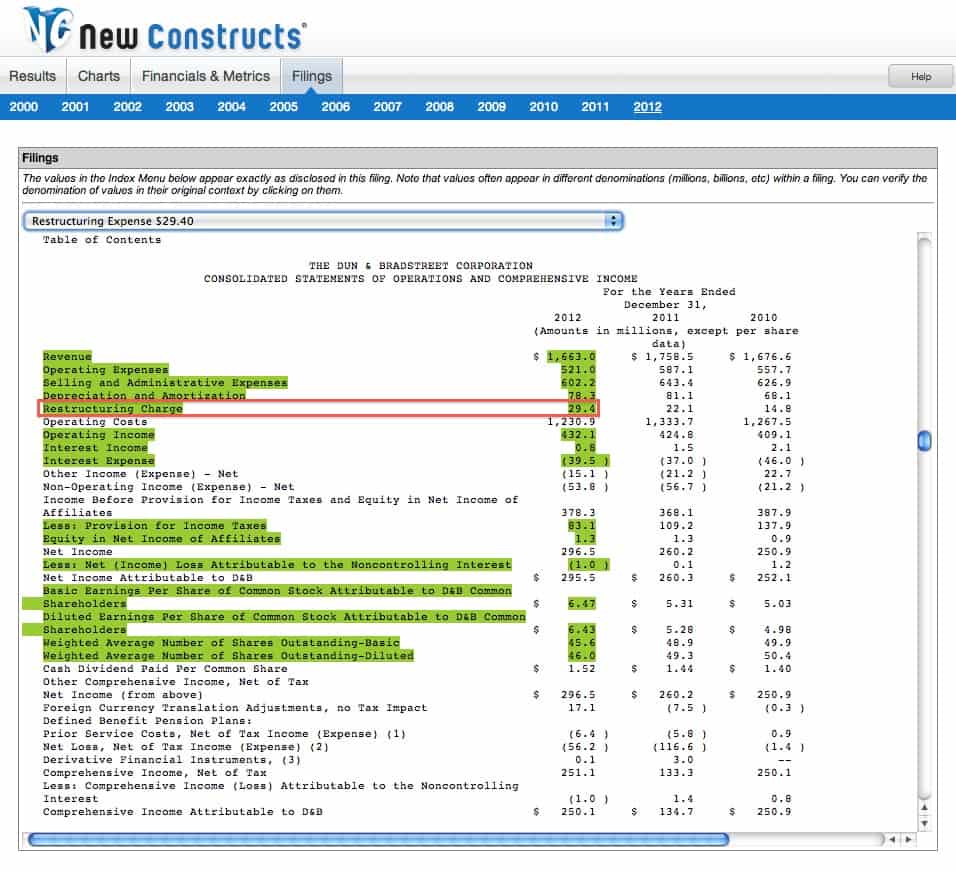

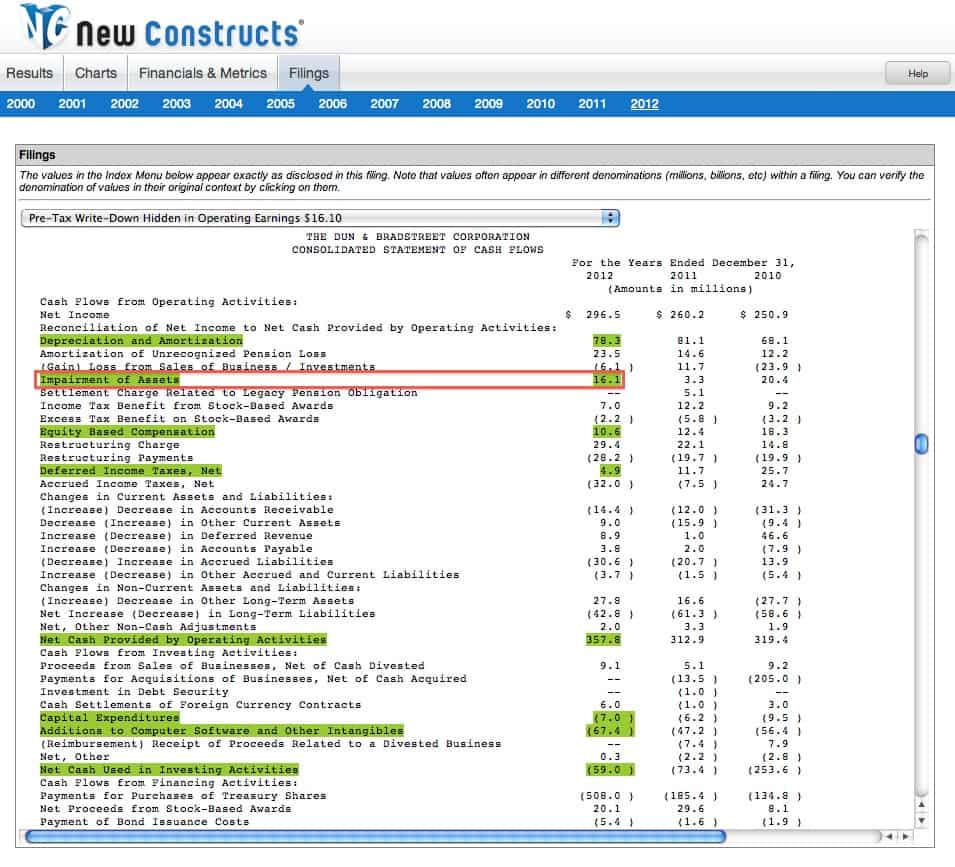

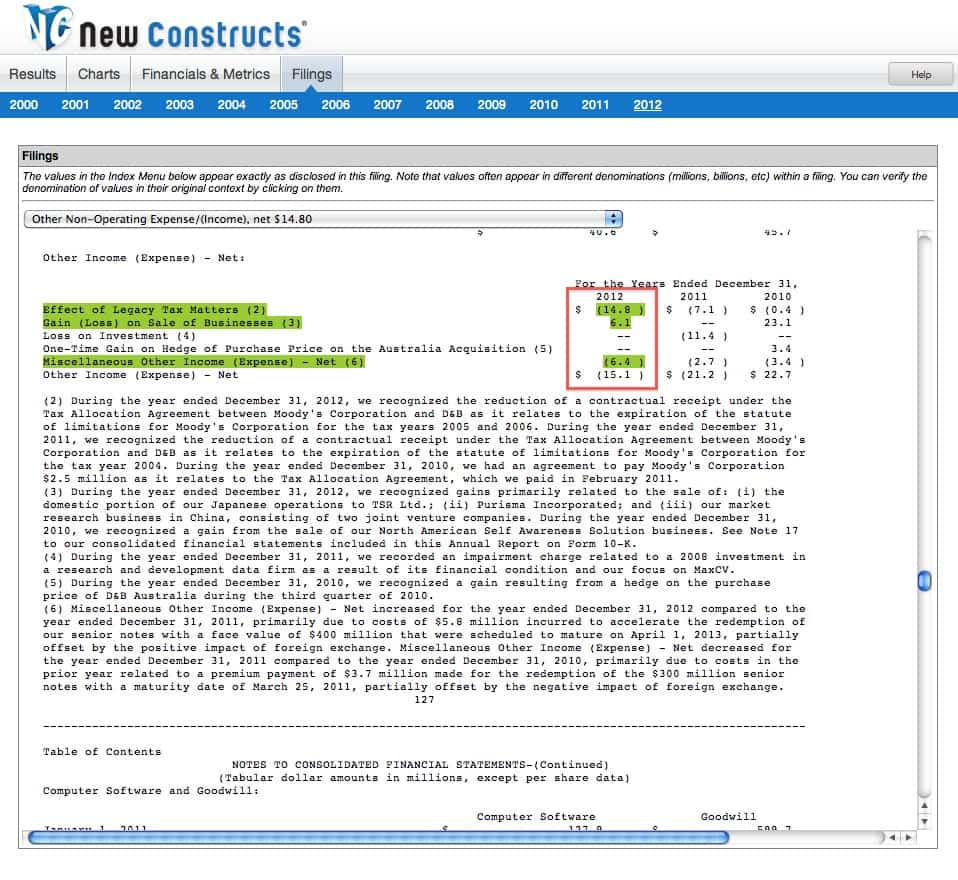

DNB’s 2012 GAAP net income significantly understates the company’s true profitability. Our NOPAT metric removes unusual non-operating expenses such as: 1) $15 million to shut down its China “Roadway” business 2) $30 million in restructuring charges 3) $16 million in write-downs, and 4) $15 million in various non-operating losses buried in “other income”. All told, DNB’s 2012 NOPAT of $370 million was 25% greater than its reported earnings.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

DNB is the largest provider of commercial data and business information. The company’s unparalleled database (with over 225 million business records) gives it a competitive edge. The demand for data increases every day, and DNB is one of the largest data providers in the world. The company’s 22%NOPAT margin in 2012, its highest margin of the millennium, attests to its ability to leverage and profit from its data.

The good news for investors is that DNB recently became a whole lot cheaper. The stock price has declined by 5% over the past 20 days due to negative coverage from Goldman Sachs (GS). Now valued at only ~$102/share, DNB has a price to economic book value ratio of 1, which means the market expects absolutely no future growth from the company. Goldman Sachs expects lower than expected EBITDA growth from DNB, but at its current valuation the stock price should appreciate with even small growth. Over the long-term, this is a strong company in a growing industry that should easily surpass the market’s low expectations for it.

Most Dangerous Stock Feature for October: SINA

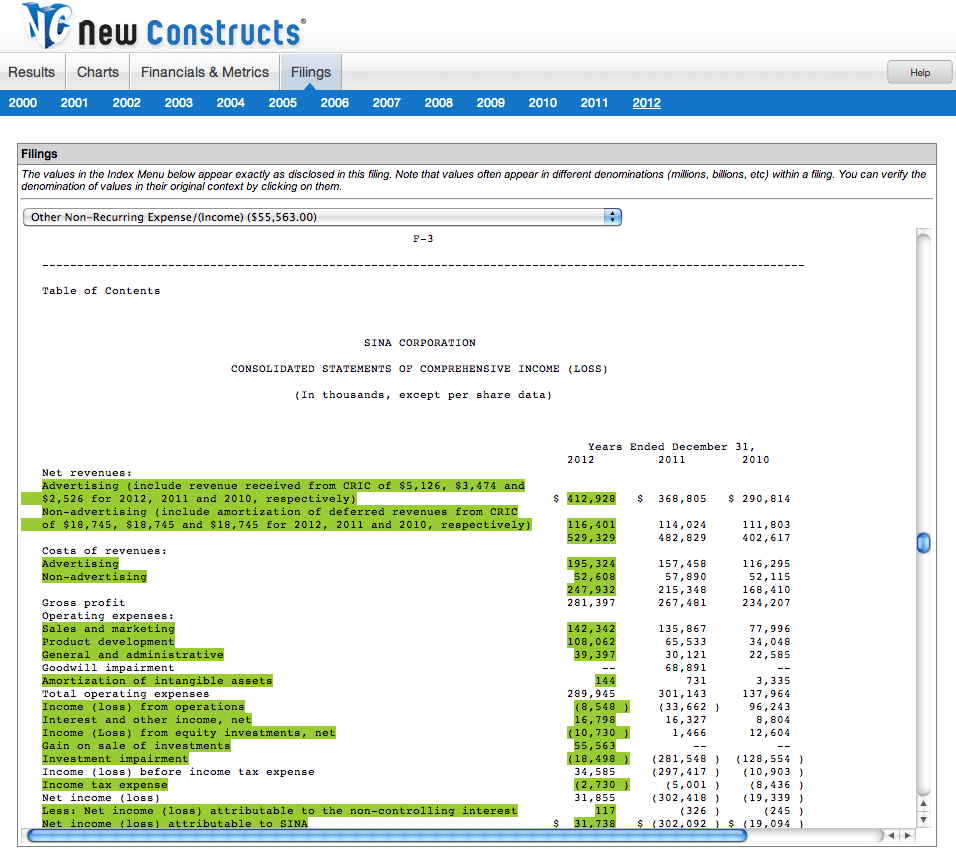

Chinese online media company Sina (SINA) is one of the new additions to the Most Dangerous list this month. SINA made the list due to the 2.2% stock price increase in September that made its valuation even riskier.

SINA’s business has struggled recently. After earning double digit returns on capital for eight straight years from 2003-2010, SINA’s ROIC declined to just 5% in 2011 and fell to -2% in 2012. SINA continues to grow revenue, but its expenses are growing much more rapidly. Its costs of revenue have tripled since 2007, and its “sales and marketing” and “general and administrative” expenses nearly doubled between 2010 and 2012. In those two years, total revenues only increased by 42%.

The company’s misleading GAAP earnings obscure the impact of expenses rising so much faster than revenue. By misleading, we refer to the fact that SINA reported a profit of $32 million in 2012 while after-tax cash flow (NOPAT) was -$18 million and economic earnings were a dismal -$92 million. The company manufactured positive results by including unusual, non-operating items in its results. SINA earned $55 million in income from the sale of its equity investments in various companies. The removal of this and other non-operating items reveals the underlying cash flows of SINA’s business to be much worse than the accounting results suggest.

{kind=link}

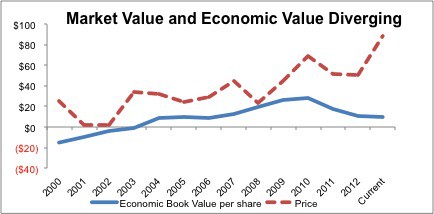

To make matters worse, SINA is richly valued at ~$88/share – near an all-time high price-to-economic book value ratio. Figure 1 shows the relationship between SINA’s stock price and its economic book value (zero-growth value) since 2000.

Figure 1: Price vs EBV

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

As you can see, the gap between SINA’s market valuation and its economic book value is more pronounced than it has been at any point since 2000. The company currently has a price to economic book value of 9, well above the threshold of 3.5 that we classify as Very Dangerous.

To justify its market valuation, SINA would need to improve its ROIC from -2% last year to nearly 50% while also growing revenues at 20% compounded annually for almost 20 years. In short, the market expects the company to quickly return to its peak profitability while also growing the business at a torrid pace. Even if they do get the business turned around, it is a little difficult betting on the company to exceed the current market expectations. Online media is a rapidly changing business with low barriers to entry and high competition. SINA can’t expect to stay on top in China forever. Even if it does continue to grow revenues, the company needs to show it can keep costs under control before it starts to look like a viable investment. Right now, its high valuation and negative profits land SINA on our Most Dangerous list.

The Most Dangerous Stocks report for October can be purchased here, while the Most Attractive Stocks can be purchased here. To gain access to these reports one week earlier each month, e-mail us at[email protected] to request a subscription.

Sam McBride contributed to this report.

Disclosure: David Trainer owns DNB. David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.