Finding the best mutual funds is an increasingly difficult task in a world with so many to choose from.

You Cannot Trust Mutual Fund Labels

There are at least 980 different large cap blend mutual funds and at least 6100 mutual funds across all styles. Do investors need that many choices? How different can these thousands of mutual funds be?

Even in the least popular style, mid cap value, there are 182 separate mutual funds. These mutual funds vary widely in the number and type of holdings they have. For example, Artisan Mid Cap Value Fund (APHQX), Harbor Mid Cap Value Fund (HAMVX), and BMO Mid Cap Value Fund (MRVIX), three of my top rated mutual funds for this style, share none of their top five holdings.

The same is true for the mutual funds in any style, as each offers a very different mix of good and bad stocks. Some styles have lots of good stocks and offer lots of good mutual funds. The opposite is true for other styles, while some styles lie in between with a fair mix of good and bad stocks. For example, large cap growth, per my 2Q Style Rankings report, ranks fourth out of 12 styles when it comes to providing investors with quality mutual funds. Large cap blend ranks first once again, and small cap value ranks last. Details on the Best & Worst mutual funds in each style are here.

The bottom line is: Mutual fund labels do not tell you what kind of stocks you are getting in any given mutual fund. This fact applies equally to index funds too. See “Danger Zone: Passive Investors” for more details.

Paralysis By Analysis

I firmly believe mutual funds for a given style should not all be that different. I think the large number of large cap blend (or any other) style of mutual funds hurts investors more than it helps because too many options can be paralyzing. It is simply not possible for the majority of investors to properly assess the quality of so many mutual funds, even in a single style. Analyzing mutual funds, done with the proper diligence, is far more difficult than analyzing stocks because it means analyzing all the stocks within each mutual fund.

Any investor worth his salt knows that analyzing the holdings of a mutual fund is critical to finding the best mutual fund.

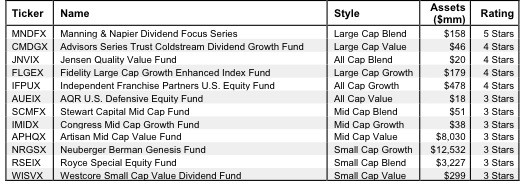

Figure 1: Best Mutual Funds By Style

Sources: New Constructs, LLC and company filings

The Danger Within

Why do investors need to know the holdings of mutual funds before they buy? They need to know to be sure they do not buy a mutual fund that might blow up. Buying a mutual find without analyzing its holdings is like buying a stock without analyzing its business and finances. As Barron’s says, investors should know the Danger Within. No matter how cheap, if it holds bad stocks, the mutual fund’s performance will be bad.

PERFORMANCE OF MUTUAL FUND’S HOLDINGS = PERFORMANCE OF MUTUAL FUND

Finding the Style Mutual Funds with the Best Holdings

Figure 1 shows my top rated mutual fund for each style. Importantly, my ratings on mutual funds are based primarily on my stock ratings of their holdings. My firm covers over 3000 stocks and is known for the due diligence we do for each stock we cover. Accordingly, our coverage of mutual funds leverages the diligence we do on each stock by rating mutual funds based on the aggregated ratings of the stocks each fund holds.

Manning & Napier Dividend Focus Series (MNDFX) is the top-rated large cap blend mutual fund and the overall top-rated fund of the 6100 style mutual funds I cover. Only the large cap blend, large cap value, large cap growth and all cap blend styles contain any Attractive (i.e. 4-star) rated mutual funds while the best every other style can offer is a Neutral or 3-star fund.

Sometimes, you get what you pay for.

It is troubling to see one of the best style mutual funds, Advisors Series Trust Coldstream Dividend Growth Fund (CMDGX) have just $46 million in assets. The largest mutual fund in large cap value, Dodge & Cox Stock Fund (DODGX), has $45 billion in assets, thought it only gets a Neutral (3-star) rating. DODGX’s total annual cost (TAC) at 0.60% is lower than PKW’s at 1.52%, but as I state above, no matter how cheap a mutual fund, if it does not hold good stocks it will not perform well. Sometimes, you get what you pay for.

Another example of how you sometimes get what you pay for: T. Rowe Price Institutional Large Cap Growth Fund (TRLGX). TRLGX has over $6.4 billion in assets despite getting a Dangerous (2-star) rating. Investors seem to be attracted to its low TAC of 0.71% with less regard for the quality of its holdings. Meanwhile, the top-rated large cap growth mutual fund, Fidelity Large Cap Growth Enhanced Index Fund (FLGEX), has a 4-star rating but only $179 million in assets.

I cannot help but wonder if investors would leave TRLGX if they knew that it has such a poor portfolio of stocks. It is cheaper than FLGEX, but as previously stated, low fees cannot growth wealth, only good stocks can.

Sometimes, you DON’T get what you pay for.

This is especially true for mutual funds, as their costs can be harder to discern than those of ETFs. While the only significant costs for ETFs are expense ratios, investors have to factor in front-end load and transaction costs to determine the true cost of a mutual fund.

Take Quaker Strategic Growth Fund (QUAGX) for example. QUAGX has over $169 million in assets with total annual costs of 5.12%, a Neutral portfolio management rating, and a Very Dangerous rating overall. Compare this to another large cap growth fund, Barrett Growth Fund (BGRWX), with an Attractive portfolio management rating and costs of 1.43%. One would think this fund would attract more investors than QUAGX, but BGRWX has just $14 million in assets. Sometimes you do not get what you pay for.

Investors should aim to avoid high fees, especially when they are paired with inferior management. There are plenty of funds that offer quality holdings for low prices: Vanguard Dividend Growth Fund (VDIGX) has both an Attractive portfolio management rating and low annual costs of 0.37%.

Along with quality holdings and low fees, liquidity is an important factor in picking mutual funds. I recommend investors only buy mutual funds with more than $100 million in assets. You can find more liquid alternatives for the other funds on my free ETF and mutual fund screener.

Covering All The Bases, Including Costs

My mutual fund rating also takes into account the total annual costs, which represents the all-in cost of being in the fund. While, my ratings weight the quality of holdings more heavily than these costs, those funds that do charge abnormally high funds to investors are penalized.

Top Stocks Make Up Top Mutual Funds

One of my favorite holdings in Coldstream Dividend Growth Fund (CMDGX) is AFLAC, Inc. (AFL), which gets my Very Attractive (5-star) rating. AFL has an impressive track record of growth over long periods of time. Since 1998, it has grown after-tax profit (NOPAT) by 14% compounded annually. On top of this, AFLAC has maintained a high return on invested capital (ROIC) every year. Since the beginning of my model in 1998, ALF’s ROIC never dips below 13% and currently sits at 19%. Despite this track record of growth and stability, its valuation of ~$56.80/share gives it a price to economic book value ratio of only 1.0. This valuation implies that the company will never grow its profits from their current levels. A track record of profitability combined with a low valuation means an attractive risk/reward for investors. Allocating a place in its top five holdings for AFL helps to explain why CMDGZ gets my Attractive rating.

Accenture PLC (ACN) is one of my favorite holdings in Advisers Investment Trust: Independent Franchise Partners US Equity Fund (IFPUX). ACN has been a model of consistency, growing NOPAT by 13% compounded annually for the past decade. Its ROIC over that time has never dipped below 30% and currently sits at an impressive 65%. As I’ve previously written, ACN’s business model puts it in an ideal position to profit off of innovation around the world without the pressure to innovate itself, and its superior human capital gives it a competitive advantage in its industry. One would expect a company with ACN’s track record of profitability and growth to have an expensive stock, but that is not the case. At its current valuation of $80.41/share, ACN has a price to economic book value ratio of only 1.1, implying that it will never grow NOPAT by more than 10% from its current level for the remainder of its corporate life. Solid fundamentals and a cheap valuation means ACN should be set to reward investors, including those invested in IFPUX.

André Rouillard and Sam McBride contributed to this report.

Disclosure: David Trainer owns ACN. David Trainer, André Rouillard and Sam McBride receive no compensation to write about any specific stock, sector, or theme.