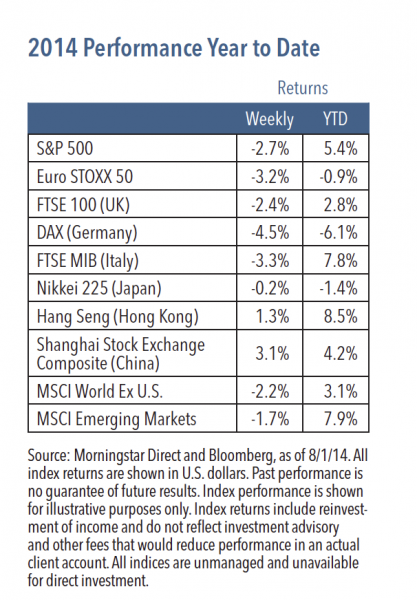

U.S. equities experienced a sharp pullback last week, with the S&P 500 Index falling 2.7%, its largest weekly decline in over two years. (1) A number of factors contributed to the downturn, including rising geopolitical tensions, concerns over Federal Reserve policy, Argentina’s debt default, a slowdown in the housing recovery and a sense that the market rally has been getting tired. Not all of the news was negative, however, since we also saw some strong economic and earnings data and increasing merger and acquisition activity.

Despite Rising Worries, the Backdrop Remains Steady

One particular area of concern last week was whether the Federal Reserve would become more aggressive about monetary policy given stronger economic growth and a pickup in inflation. Specifically, the second quarter gross domestic product report showed stronger-than-expected growth at 4.0%, (2) and the second quarter employment cost index rose 0.7%, its fastest pace in six years. (3)

Despite this mounting concern and a broader rise in negativity, we do not believe that much has actually changed. The economy continues to improve, the Fed is slowly moving toward normalization, earnings are strong, valuations are stable and the geopolitical environment is unsettled but not disastrous.

Weekly Top Themes

- GDP growth is indeed improving. Although some of last quarter’s growth can be attributed to a buildup of inventories (which may prove to be temporary), the economy does appear to be on more solid ground. We are continuing to forecast approximately 3% growth for the second half of the year.

- July’s labor market data was solid, with 209,000 new jobs reported. (3) This represents a slowdown compared to recent months, but is still a solid pace. Unemployment ticked up to 6.2%, but this was largely due to an increase in the participation rate as more people are reentering the workforce. (3)

- Last week’s FOMC meeting produced little in the way of any real change, but the policy debate is starting to churn beneath the surface.

- Manufacturing data continues to impress. July’s ISM Manufacturing Index was positive, with new orders, employment and production all rising. (4)

- Earnings growth remains strong. More than 70% of companies have reported results, with 75% beating earnings expectations and two-thirds beating revenue forecasts. (5) At this point, it looks like second quarter earnings growth should be up around 9%.

- Sanctions against Russia should result in limited economic risk to the United States. The turmoil in Ukraine presents geopolitical risks, but as of now should have little impact on U.S. growth.

- Market technicals are becoming sloppy. The S&P 500 Index hit new highs four times in July, and each time more stocks actually declined than advanced. (1) This technical backdrop is another reason we are concerned about the possibility of a market correction.

We Expect a Choppy Third Quarter, but Believe Investors Should Continue to Hold Overweight Positions in Equities

With so many potential triggers for a market correction, we think the likelihood of a pullback in equity prices is growing, and we expect investors may experience a bumpy ride in the coming months. We do not believe a bear market is in the works, however. Bear markets tend not to develop unless a recession or a collapse in earnings is imminent, and today both economic and earnings growth are improving.

As such, we do not believe it would make sense for investors to scale back on equities and move to the sidelines. Volatility appears to be rising and we could see additional pullbacks, but trying to time the markets is a losing proposition. Over the next year, we expect equity markets to produce returns in the high single digits, while some areas of the bond market may struggle in the face of rising rates. Therefore, we continue to recommend an overweight investment stance in equities over bonds.

(1) Source: Morningstar Direct, as of 8/1/14.

(2) Source: Bureau of Economic Analysis.

(3) Source: Bureau of Labor Statistics.

(4) Source: Institute of Supply Management.

(5) Source: RBC Capital Markets.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

Robert C. Doll, CFA is Chief Equity Strategist and Senior Portfolio Manager for Nuveen Asset Management. Follow @BobDollNuveen on Twitter.