Serving retirement income clients is not a new activity for advisors. According to our research on best practices in retirement income delivery that has involved continuously interviewing and surveying advisors since 2008, more than nine in 10 advisors across channels have at least 20 percent of their current clients nearing or in retirement. Yet even as the much anticipated shift of boomers to retirement has begun in earnest, only a limited number of advisor practices—an estimated 5,000 or fewer from our analysis—are today directing their efforts primarily to serve retirement income clients. Why is it that more advisors have yet to embrace retirement income and orient their practices to supporting this growing audience?

There are a number of factors that have caused advisors to not fully embrace the retirement income opportunity. Many advisors mistakenly believe that retirement income clients are a diminishing asset, not recognizing that these clients tend to consolidate investments and to be more loyal. Advisors have yet to experience, or have not fully recognized negative impact as far as lost clients and assets by not shifting more efforts toward retirement income. Other advisors do not fully understand the distinctions involved in retirement income support, believing that servicing for these clients is indistinct from support for accumulation-focused clients. In addition, many advisors are challenged by other priorities or day-to-day demands in their practices and have not thought strategically about how to align with a client base that is changing over time.

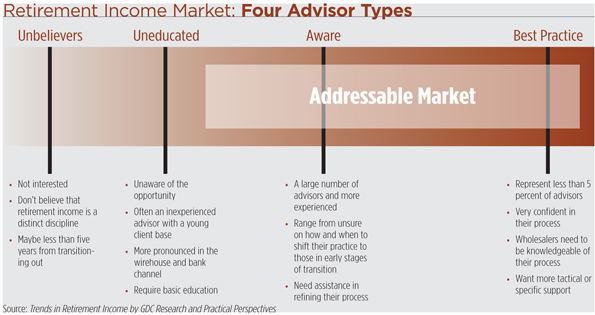

To provide perspective on the nature of retirement income delivery and how advisors are evolving their practices, we have identified four distinct prototypes that comprise the retirement income marketplace:

• Unbelievers, or those advisors who have yet to embrace retirement income and remain disengaged from actively supporting clients in this space.

• Uneducated, or those advisors who are broadly familiar with the opportunity but who have not yet invested the time or resources to develop the deeper knowledge, skills or capabilities to serve retirement income clients in a more active and engaged fashion.

• Aware, or those advisors who comprehend the opportunity in serving income clients and are transitioning their practices to more actively serve distribution-focused clients.

• Best practice, or those advisors who are already deeply rooted in serving income clients and position themselves to clients as retirement experts with a full range of skills and a broad scope of capabilities and services.

Given the various practice prototypes, it is not surprising that significant differences exist in how advisors serve retirement income clients. Most advisors have some form of income process to guide client support, with steps that include information discovery and data gathering, an income needs versus sources gap analysis, a projection of future sustainability of the income and overall portfolio, recommendations on new solutions to be considered, implementation of income and risk management solutions, and periodic monitoring, review and adjustment of the plan and tactics. The formality of this process and related planning varies widely among advisors, ranging from “yellow pad,” conversational-based assessments and plan development to highly formalized, comprehensive planning and forecasting using sophisticated software packages.

There is also wide variation in how advisors manage client portfolios to meet retirement income needs. Advisors serving retirement income clients generally must try to achieve multiple objectives, working to find a balance among generating sustainable income, preserving capital, and maintaining long-term purchasing power over extended life spans. The focus of the advisor must extend beyond just the rate of return or yield, taking into account the different variables and risks associated with retirement. Consequently, there is no agreed-upon framework or philosophy that is being implemented as best practice for managing income delivery. Instead, our research has identified three core philosophies that advisors use for retirement income, summarized as follows:

• Risk-adjusted total return approach, with a focus on optimizing total return within client risk parameters and periodically drawing off income or cash flow to meet spending needs;

• Pooled or bucket approach, with an emphasis on managing assets across duration-based short, intermediate, and long-term sub-accounts or pools, with an emphasis on using guaranteed solutions as part of the portfolio;

• Hybrid or income floor approach, with the goal of providing assured income for client non-discretionary “needs” by using guaranteed or short-term investments while managing the remainder of the portfolio for optimal return to meet discretionary “wants.”

In serving retirement income clients, advisors are facing a number of significant challenges. Two in three, according to our research, agree that managing investment risk is more of a challenge now in serving income clients. In addition, advisors are facing an unprecedented low yield environment that has challenged their ability to meet income needs. Again, nearly two in three advisors agree that generating income for clients is increasingly difficult given the lingering low yields on traditional fixed income and bank solutions. The challenges of risk and low yields are further compounded by rising client concerns of outliving their assets and being able to sustain sufficient income for 10, 20 or 30 years or more in retirement.

So, are we there yet? The answer is yes, the retirement income opportunity is here. The focus on retirement income has been a boon for those early adopter advisors, but what about the rest? While most advisors are confident in their abilities to help clients, they are also looking over their shoulder, seeking validation that they are following the appropriate path for clients. Advisors are aware they need to make changes and are open to new ideas, products, and solutions to serve retirement income clients, but they want more certainty and proof that these are effective before changing their approach.

Today’s advisors don’t have the luxury like their predecessors of developing a retirement income process slowly over the course of a decade or more. They are increasingly looking to third-party sources including peers, asset managers, platform providers, insurers, broker/dealers, and RIA custodians to provide a starting framework and help them gain a better understanding of strategies, tactics and processes they can employ to better serve income clients.

Dennis Gallant, president of GDC Research and Howard Schneider, president of Practical Perspectives, are two independent consultants and researchers that cater to the retirement income market. The authors’ blog, titled Approaching Retirement, will launch on WealthManagement.com in the first quarter of 2013.