Limitations on the deductibility of investment advisory expenses can have outsized impact on taxpayers with high adjusted gross incomes (AGI) or those subject to the alternative minimum tax (AMT). Taken together, the 2 percent of AGI limitation and the overall limitation on itemized deductions (imposed by Sections 67 and 68, respectively) limit the deductions taxpayers are entitled for investment advisory expenses. While the limitations set forth in these Sections affect all taxpayers, the impact increases in magnitude as AGI rises, effectively, raising tax rates for those taxpayers. Additionally, the AMT limitations (imposed by Section 56) operate to prevent taxpayers subject to the AMT from taking any deduction with respect to Section 212 expenses (expenses for the production of income). The following examples illustrate these limitations. The examples focus on individual taxpayers; however, the same result follows for non-grantor trusts and estates under Section 67 (Section 68 doesn’t apply to estates).

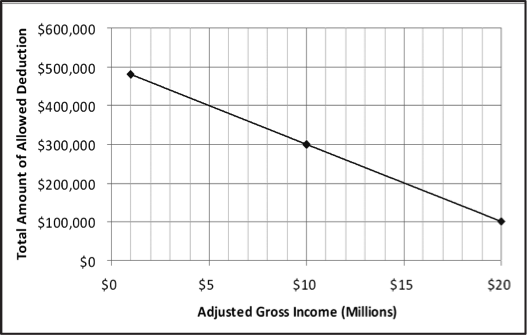

Impact of the 2 Percent Floor as AGI Increases

The taxpayer in the examples below holds a variety of investments and hires an investment advisor but is not engaged in a trade or business. The investment advisory fee is $500,000 in each example. These expenses are appropriately characterized as miscellaneous itemized deductions subject to the 2 percent floor. For illustration purposes, the impact of the AMT is not considered, as it is addressed separately below.

Example 1:

- AGI: $1,000,000

- $20,000 disallowed

- $480,000 deduction allowed

Example 2:

- AGI: $10,000,000

- $200,000 disallowed

- $300,000 deduction allowed

Example 3:

- AGI: $20,000,000

- $400,000 disallowed

- $100,000 deduction allowed

The graph illustrates the impact of the 2 percent floor as AGI increases: The taxpayer with an AGI of $1,000,000 only loses 4 percent of the deduction for investment advisory expenses, whereas the taxpayer with an AGI of $20,000,000 loses 80 percent of the deduction.

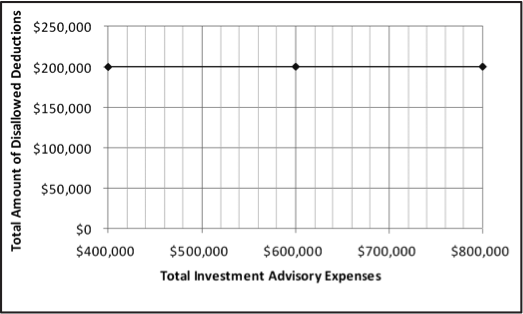

Impact of the 2 Percent Floor as Miscellaneous Itemized Deductions Increase

The following graph illustrates the impact of the 2 percent floor as investment advisory expenses increase, with a static AGI of $10,000,000. Regardless of the increase in expenses, the deduction disallowed remains static, so long as the AGI also remains static.

Impact of the Overall Limitation on Itemized Deductions

Section 68(a) reduces the allowable deduction by the lesser of 3 percent of AGI above the specified base or 80 percent of allowable deductions. The applicable base in 2016 is $258,250 for a single taxpayer.

In Example 3, if all facts remain the same, Section 68(a) further limits the deduction by $80,000 (80 percent of allowable deductions). The taxpayer would only be entitled to deduct $20,000 of the $500,000.

AMT

In Example 2, without the AMT, the taxpayer would be able to deduct $300,000 of the $500,000 investment expense. However, because the taxpayer is subject to the AMT, all $500,000 will be disallowed, and the taxpayer would be able to deduct none of it.

The limitation on deductibility of investment advisory expenses is an issue that grows in magnitude with AGI. As AGI increases, the ability to deduct investment advisory expenses diminishes significantly. If the AMT is applicable, the deduction may be disallowed entirely. Advisors should work with their clients to determine what expenses are subject to the limitations, monitor the impact of these limitations and develop strategies to minimize the impact.