This report is one of a series on the adjustments we make to convert GAAP data to economic earnings.

Reported earnings don’t tell the whole story of a company’s profits. They are based on accountingrules designed for debt investors, not equity investors, and are manipulated by companies to manage earnings. Only economic earnings provide a complete and unadulterated measure of profitability.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

Non-operating expenses are unusual charges that don’t appear on the income statement because they are bundled in other line items. Without careful footnotes research, investors would never know that these non-recurring expenses distort GAAP numbers by lowering operating earnings. Examples of hidden non-operating expenses include: restructuring or severance costs, litigation costs and certain pension costs/income. Another hidden non-operating item is asset write-downs to which we dedicate a separate report.

Our models remove this distortion to reveal a company’s recurring, core, net operating profit after tax: NOPAT.

Verizon Communications’ (VZ) $7.6 billion pension adjustment in 2012 is a prime example of the distorting effect that hidden non-operating expenses have on a firm’s GAAP earnings. That non-recurring charge, along with other hidden expenses caused VZ’s GAAP earnings to decline to $875 million while its NOPAT was $20.4 billion.

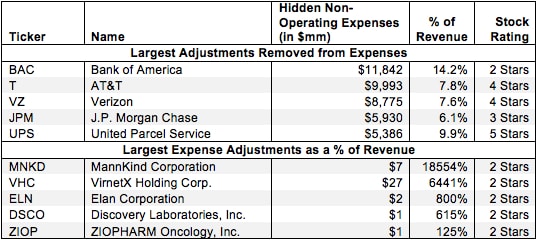

Figure 1 shows the five companies with the largest (gross value and as a % of revenue) non-operating expenses adjusted out of NOPAT for 2012.

Figure 1: Biggest Offenders for Non-Operating Expenses Hidden in Operating Earnings in 2012

Sources: New Constructs, LLC and company filings

Sources: New Constructs, LLC and company filings

The ten companies in Figure 1 are not the only offenders. In the last fiscal year, New Constructs found 9,188 non-operating expenses hidden in operating earnings for 2,032 different companies. Our database contains over 34,000 non-operating expenses that we remove from reported operating earnings for a total adjustment value of over $453 billion.

Though the removal of non-operating expenses can increase NOPAT, it does not always mean the company’s stock will earn a favorable rating. For instance, all five of the companies in Figure 1 with the highest levels of adjustments as a percentage of revenue get a 2-star, or Dangerous rating. Despite our removal of large amounts of expenses, all five of those companies still had a negative NOPAT in 2012.

In other cases, however, non-operating expenses can artificially depress reported earnings and make a stock look overvalued. Case in point: United Parcel Service (UPS) from Figure 1 had a total of $5.3 billion (or 97% of its economic earnings) in non-operating expenses in 2012 due to certainunusual pension costs. Removing these unusual charges raised UPS’s NOPAT to $7.5 billion versus its unusually low GAAP net income of $807 million in 2012.

{kind=link}

Based on GAAP earnings alone, UPS looks overvalued. The economics of the business tell a different story. The stock currently trades at a price to economic book value ratio of 0.8. That ratio means the market expects UPS’ NOPAT to permanently decline by 20%. Those are low expectations for a business that has grown NOPAT at 10% compounded annually over the past 12 years.

Without careful analysis of footnotes and the MD&A, investors do not get the complete picture of UPS. Diligence pays.

Sam McBride and André Rouillard contributed to this report.

Disclosure: David Trainer owns VZ. David Trainer, Sam McBride and André Rouillard receive no compensation to write about any specific stock, sector, or theme.